Choosing between YNAB and Monarch Money isn’t really a question of which app has better features; it’s a question of which financial philosophy matches who you actually are. Both apps cost nearly the same amount. And both connect to your bank accounts. Additionally, both have strong mobile apps and respectable reputations. But they’re built around fundamentally different beliefs about what makes people better with money, and if you pick the one that doesn’t match your money personality, you’ll abandon it within a month regardless of how well-designed it is. That’s the mistake most comparison articles skip entirely, and it’s why so many people have paid for both apps only to end up using neither consistently.

This guide cuts straight to what actually matters: the philosophy difference that determines which app will work for your specific financial situation, an honest feature-by-feature breakdown, the real pricing picture, and a direct verdict for every type of user. Whether you’re drowning in debt and need a system that forces behavioral change, coming from Mint and looking for a replacement, or building wealth and want everything in one dashboard, you’ll leave this guide knowing exactly which app belongs on your phone.

A note before we begin: every YTC score is earned, never negotiated. If you want to understand exactly how we evaluate apps & tools, our Review Methodology lays it all out.

YNAB vs Monarch: The Core Philosophy Difference

Before looking at a single feature, you need to understand this distinction because it determines everything else about which app will stick for you.

YNAB

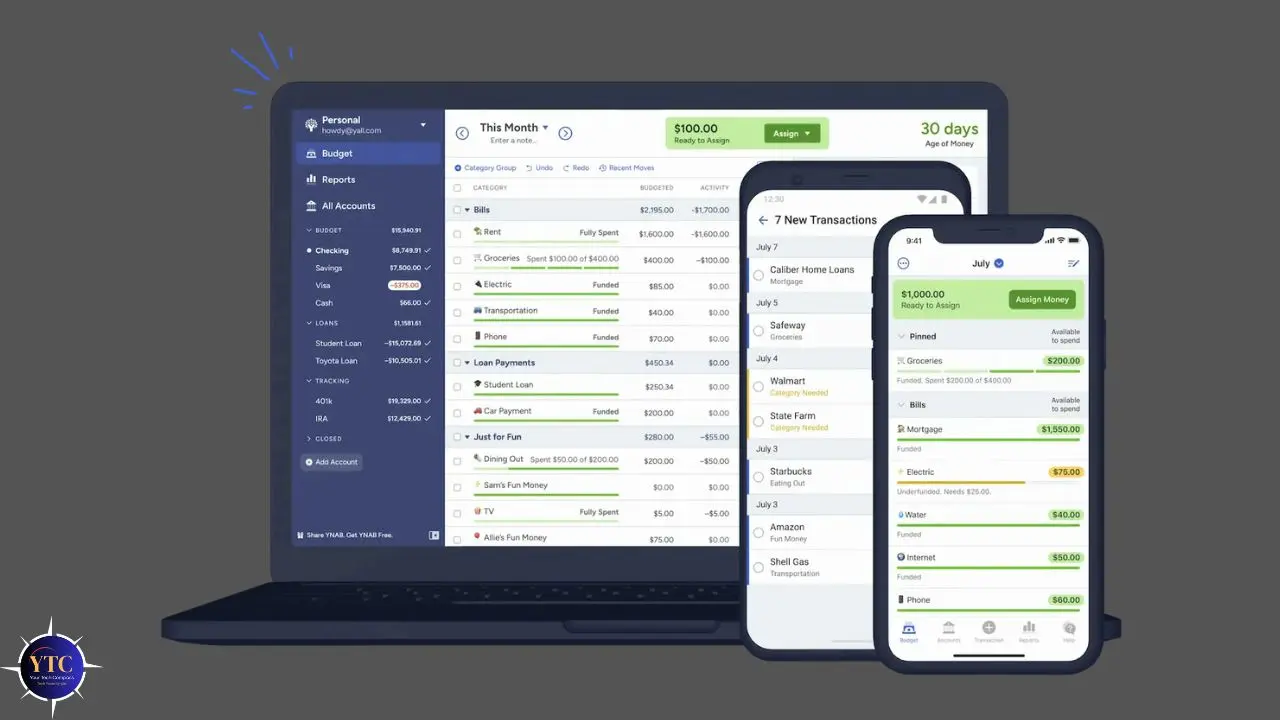

YNAB is built around zero-based budgeting, a system in which every dollar you earn is assigned a specific job before you spend it. You’re not tracking what you already spent; you’re deciding in advance where every dollar is going.

When your paycheck hits, you open YNAB and allocate it: this much to rent, this much to groceries, this much to the car repair fund you’ve been ignoring. When you overspend in one category, you don’t just note the overage.

You move money from another category to cover it, which forces a real-time decision about your priorities. The result is that YNAB makes your financial decisions feel intentional and visible rather than accidental and invisible. That intentionality is what changes behavior, and behavior change is YNAB’s entire product.

Monarch Money

Monarch Money is built around automated financial aggregation; the belief that reducing friction and providing comprehensive visibility helps people improve their financial situation. You connect all your accounts, Monarch pulls in transactions automatically, categorizes them using machine learning, and gives you a complete picture of your financial life: spending trends, net worth, investments, debts, cash flow, and savings goals, all in one dashboard.

You set spending targets per category, Monarch tracks your progress, and you review rather than actively manage. The philosophy is that clarity and awareness, delivered with minimal friction, are what make financial management sustainable for most people. Consequently, Monarch works like a financial co-pilot (it shows you where you are so you can make better decisions), while YNAB works like a financial trainer that requires you to show up and do the work.

The Implication

The practical implication of that difference is direct: if you need to fundamentally change your spending behavior to get out of debt or stop living paycheck to paycheck, YNAB’s active engagement requirement is a feature, not a flaw; the friction is what produces the behavioral change.

If your spending is generally under control and you primarily want clear visibility into your complete financial picture, Monarch’s low-friction approach delivers that without the daily commitment YNAB requires. Picking the wrong one for your situation is like hiring a personal trainer when you wanted a nutritionist; both are legitimate and effective, but neither helps you if it doesn’t match your actual problem.

What Is YNAB?

YNAB (You Need A Budget) was founded in 2004 by Jesse Mecham, making it one of the oldest and most established personal finance apps on the market. That longevity matters because YNAB has spent two decades refining a specific methodology rather than just a software product.

The four rules at the core of the system are: Give Every Dollar a Job (assign every dollar to a category before spending it), Embrace Your True Expenses (break large irregular expenses like car repairs and annual subscriptions into monthly amounts so they don’t blindside you), Roll With the Punches (when you overspend in a category, adjust rather than abandon the budget), and Age Your Money (the long-term goal of paying this month’s bills with last month’s income rather than living paycheck to paycheck).

Together, these four rules form a complete financial philosophy, not just a set of app features, which is why YNAB has a support ecosystem of workshops, webinars, YouTube content, certified coaches, and an active user community that no competing budgeting app comes close to matching.

YNAB is available on iOS, Android, and web browsers. Pricing is ~$14.99/month or ~$109/year, as confirmed on YNAB’s official pricing page. The 34-day free trial requires no credit card, making it one of the most generous evaluation periods among paid budgeting apps.

College students get one free year. There is no permanent free tier. The app allows up to 6 people to share one subscription; useful for families, though all users share the same login credentials rather than having separate profiles. YNAB’s data shows users save an average of $600 in their first two months and $6,000 in their first year, a return on investment that makes the $109 annual cost straightforward to justify for users who commit to the methodology.

What Is Monarch Money?

Monarch Money was founded in 2019 by Val Agostino (a former Mint executive) and a team of former Mint engineers who built Monarch specifically to be the product Mint should have become before Intuit neglected and eventually shut it down in January 2024. That context explains a lot about Monarch’s design philosophy: it delivers the automated, low-friction financial tracking that Mint users loved, then adds the investment tracking, net worth dashboard, and collaborative features that Mint never built. Consequently, when Mint shut down, Monarch became the primary destination for millions of displaced users seeking a comparable product with added depth, and Monarch’s user base grew substantially.

Monarch connects to over 13,000 financial institutions as of March 2026, including banks, credit cards, investment accounts (401(k), IRAs, brokerage accounts), mortgages, loans, and property values, giving you a genuinely complete financial picture in one dashboard. Pricing is ~$14.99/month or ~$99.99/year, as confirmed from Monarch’s official pricing.

The 7-day free trial includes full access to all features. There is no permanent free tier. Collaboration is included at no extra charge; you invite your partner or spouse to share the same dashboard without upgrading to a separate plan. Monarch uses machine learning to categorize transactions automatically and learns your preferences over time, improving accuracy the longer you use it, with minimal ongoing correction needed.

YNAB vs Monarch: Feature-by-Feature Comparison

Budgeting System

YNAB uses zero-based budgeting with strict envelope-style category allocation; every dollar is assigned, and every overspend requires a deliberate reallocation decision. That active requirement is what makes YNAB effective for behavioral change.

Monarch uses cash-flow-based budgeting: you set monthly spending targets per category, Monarch tracks your progress automatically, and you review rather than actively manage. Monarch’s approach allows budgeting with expected future income, which YNAB’s current-money-only philosophy doesn’t support.

The honest trade-off is direct: YNAB’s system changes behavior; Monarch’s system provides awareness. Both are valuable; they solve different problems.

Account Connections and Syncing

YNAB connects to bank accounts and credit cards via Plaid; manual import is available for accounts that don’t connect automatically. Connection reliability has long been a noted limitation, though YNAB has improved it with recent updates.

Monarch connects to over 13,000 institutions, including banks, credit cards, investment accounts, mortgages, loans, and property values, and is broadly praised for connection reliability and breadth. Additionally, Monarch automatically identifies recurring subscriptions and bills and notifies you before they charge, a feature YNAB doesn’t offer. For users with diverse financial accounts across multiple institutions, Monarch’s breadth of aggregation is a meaningful practical advantage.

Net Worth and Investment Tracking

This is one of the clearest capability gaps between the two apps, and it matters significantly depending on what you need. YNAB tracks basic account balances and provides a simple net worth view, but it is not designed for managing investment portfolios. It doesn’t track investment holdings, portfolio performance, or asset allocation.

Monarch, by contrast, provides a comprehensive net worth dashboard that aggregates investment accounts, spending, debt, and assets, showing you how your overall financial picture changes over time. If you have a 401k, an IRA, a brokerage account, or any investment holdings you want to monitor alongside your budget, Monarch serves that need, and YNAB simply doesn’t. For users in the wealth-building phase of their financial journey, that distinction alone can determine the right choice.

Reporting and Analytics

YNAB produces strong budget-focused reports, including spending by category, net worth over time, and the Age of Money metric, which shows how many days old your money is (a proxy for how far ahead of your bills you are). These reports are specifically designed to support the zero-based budgeting methodology.

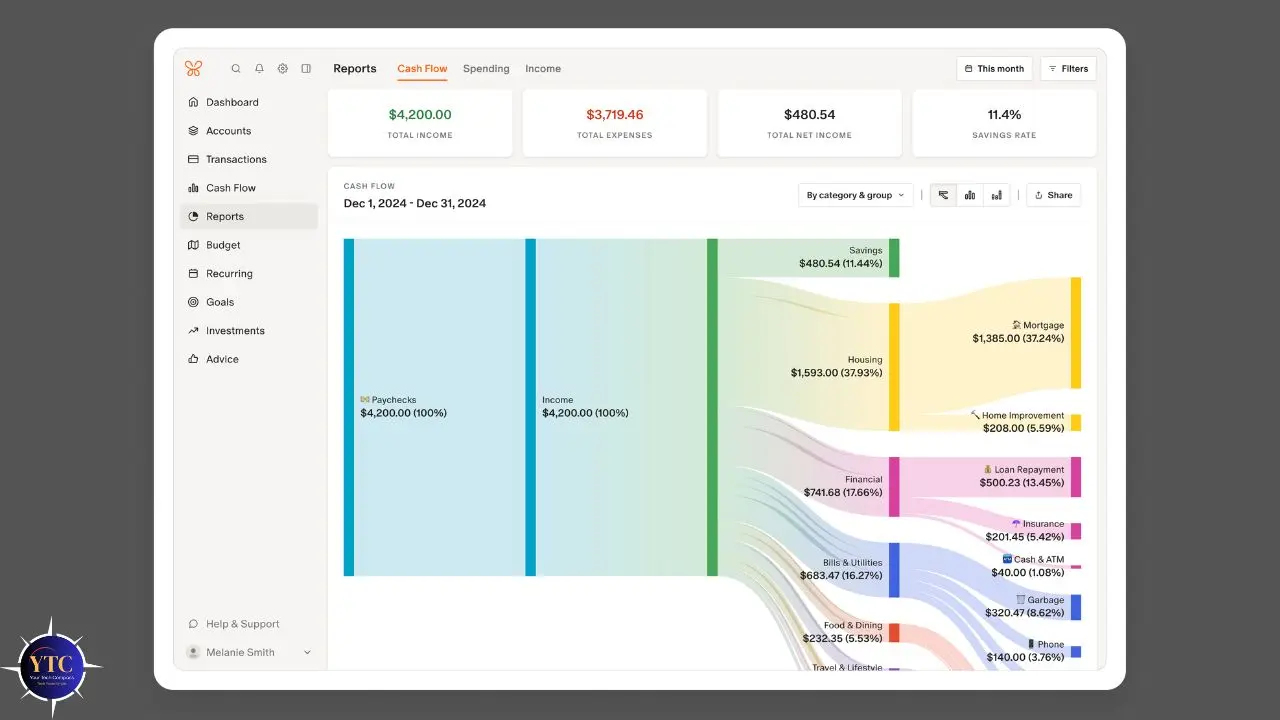

Monarch produces broader financial reports covering spending trends, income analysis, cash flow patterns, net worth growth over time, and investment performance, a more comprehensive reporting suite for users who want data-rich financial analysis beyond budget category tracking. Furthermore, Monarch includes AI-powered insights that automatically surface patterns and anomalies in your financial data.

Both reporting systems are strong. YNAB is deeper for budget-specific analysis; Monarch’s is broader for overall financial health tracking.

Debt Payoff Tools

YNAB’s approach to debt is methodological: you allocate money to debt payoff as a budget category; the system forces you to prioritize it alongside every other dollar decision; and the behavioral change that the zero-based system creates directly supports the sustained commitment that debt elimination requires. Many of YNAB’s most passionate user stories specifically involve paying off significant debt using the methodology.

Monarch includes dedicated debt-tracking and payoff-planning tools, such as a visual debt-payoff timeline and a more explicit debt-management feature than YNAB’s methodology-integrated approach. However, both apps address debt effectively, but in fundamentally different ways: YNAB through behavioral change, Monarch through explicit planning tools.

Collaborative Features

YNAB supports shared budgets for couples and families, up to 6 users on one subscription, real-time sync, and shared category management. The limitation is that all users share the same login credentials rather than having separate user profiles.

Monarch was built with couples in mind from the start; a shared financial dashboard, separate user profiles, split expense tracking, and collaborative goal setting are all included at no extra charge. In addition, shared financial management is one of Monarch’s most praised features among couples, with the separate-user-profile approach feeling more polished than YNAB’s shared-credential model.

For users exploring investment apps alongside budgeting, our Robinhood vs eToro comparison covers the investment platform side of the financial picture that Monarch tracks, but neither budgeting app actively manages it.

YNAB vs Monarch: Pricing Comparison

Feature | YNAB | Monarch Money |

Monthly Price | ~$14.99/month | ~$14.99/month |

Annual Price | ~$109/year | ~$99.99/year |

Free Trial | 34 days (no credit card) | 7 days (full access) |

Free Tier | ❌ No | ❌ No |

Users Per Plan | Up to 6 (shared login) | Partner included (separate profiles) |

Student Discount | ✅ 1 free year | ❌ No |

The pricing is close enough that it should not be the deciding factor between these two apps. At $109/year for YNAB versus $99.99/year for Monarch, the difference is approximately $9 annually; irrelevant compared to the far more important question of which app’s philosophy will actually produce results for your specific financial situation.

The free trial difference is more meaningful: YNAB’s 34-day trial gives you enough time to complete a full budget cycle and genuinely evaluate whether the methodology works for you, while Monarch’s 7-day trial is barely enough to set up your accounts and see the dashboard in action. If you’re uncertain which app is right for you, YNAB’s no-credit-card 34-day trial is a more informative way to evaluate.

Full Comparison Table

Feature | YNAB | Monarch Money |

Budgeting Method | Zero-based (proactive) | Cash flow (tracking-based) |

Free Tier | ❌ No | ❌ No |

Free Trial | ✅ 34 days | ⚠️ 7 days |

Annual Price | $109/year | $99.99/year |

Investment Tracking | ❌ Limited | ✅ Comprehensive |

Net Worth Dashboard | ⚠️ Basic | ✅ Full dashboard |

Debt Payoff Tools | ✅ Methodology-integrated | ✅ Explicit planning tools |

Couple/Family Sharing | ✅ Up to 6 users | ✅ Separate profiles included |

Auto Transaction Import | ✅ Yes | ✅ Yes |

Subscription Detection | ❌ No | ✅ Automatic |

AI-Powered Insights | ❌ No | ✅ Yes |

Educational Resources | ✅ Extensive | ⚠️ Growing |

Account Breadth | ⚠️ Banks + credit cards | ✅ 13,000+ institutions |

Mobile App | ✅ Strong | ✅ Strong |

Best For | Behavioral change; debt payoff | Financial visibility; wealth building |

Who Should Choose YNAB?

Users Carrying Debt

Users carrying debt who need to fundamentally change their spending behavior are YNAB’s clearest success story. The zero-based system makes debt payoff a deliberate, prioritized decision rather than something that happens with whatever money is left over at the end of the month, and the behavioral change it creates is especially effective for users who have been avoiding direct engagement with their financial reality. YNAB’s own data, showing $6,000 in savings in the first year, reflects this behavioral impact on users who commit to the methodology.

People Living Paycheck to Paycheck

People living paycheck to paycheck benefit from YNAB’s system because the zero-based approach forces you to confront exactly how much you have and allocate it before spending begins. That confrontation is uncomfortable, which is precisely why YNAB works where passive tracking tools don’t.

Awareness of a problem and behavioral tools to address it are different things, and YNAB provides both. Additionally, users who want a financial education ecosystem, not just software, get significantly more from YNAB’s workshops, certified coaches, YouTube channel, and active community than from any competing app.

For users managing everyday finances alongside budgeting, our Zelle app review covers one of the most widely used payment tools that integrates naturally with a YNAB budgeting workflow.

Who Should Not Choose YNAB?

- Users who want passive, low-friction financial monitoring.

- Investors who need portfolio tracking alongside budgeting.

- Users who tried YNAB before and found the daily engagement requirement unsustainable.

- Users coming from Mint who want a similar automated experience.

Who Should Choose Monarch Money?

Mint Refugees

Mint refugees are Monarch’s most natural audience; Monarch is the most direct functional replacement for Mint, built by former Mint engineers who understood exactly what made Mint popular and what it was missing. Automatic transaction import, categorization, spending trend visualization, and a familiar dashboard experience are all present, with investment tracking, net worth monitoring, and collaborative features added on top. Therefore, if you used Mint and want a comparable product that won’t be shut down, Monarch is the clear destination.

For a broader comparison of personal finance tracking apps that fills the post-Mint landscape, our Mint vs Rocket Money comparison covers another major alternative worth understanding alongside Monarch.

Investors and Wealth Builders

Investors and wealth builders who want to see their complete financial picture, savings, investments, debt, net worth trend, and spending in one place get significantly more value from Monarch than from YNAB.

Monarch’s investment account tracking, portfolio performance monitoring, and net worth dashboard make it the right choice for users in the wealth-building phase, where budgeting is just one component of a broader financial management need. Additionally, couples managing finances jointly find Monarch’s separate user profiles, shared dashboard, and split expense tracking more polished and practical than YNAB’s shared-credential approach.

Who Should Not Choose Monarch?

- Users who need to fundamentally change their spending behavior to get out of debt.

- Users who want a structured financial methodology with an educational framework.

- Users who found Mint gave them visibility without producing behavioral change; Monarch has a similar dynamic and will likely produce the same result for the same type of user.

For a broader look at the full range of financial and productivity apps worth evaluating, the apps and tools section covers the complete landscape.

Can You Use Both?

Some users do use both apps simultaneously: YNAB for active budget management and Monarch for investment and net worth tracking. That combination makes sense on paper: YNAB handles the behavioral-discipline side, and Monarch handles the comprehensive financial-visibility side.

In practice, however, paying approximately $210 per year for two budgeting apps works well only if your financial life is genuinely complex enough to need what each app provides independently, and most users find that one app covers their needs completely once they commit to using it properly. The more practical approach is to choose the app that matches your primary financial need, use it consistently for 90 days, and reassess based on real usage data rather than theoretical feature coverage.

FAQs

Monarch is easier for beginners to set up and start using. Immediately connect your accounts, see your dashboard, and you’re oriented within 20 minutes. YNAB has a steeper learning curve; new users typically spend several hours setting up their first month’s budget and learning the zero-based methodology before it feels natural. That said, YNAB’s educational resources make the learning curve manageable, and the methodology becomes intuitive quickly for users who commit to it.

Both support couples well, but Monarch’s separate user profiles, shared dashboard, and split expense tracking provide a more polished joint financial management experience than YNAB’s shared-login approach. Monarch is the stronger choice specifically for couples who want independent access to a shared financial picture without shared credentials.

Yes. Monarch is the most direct functional replacement for Mint, built by former Mint engineers who understood Mint’s strengths and limitations. It provides automated transaction import, spending categorization, trend visualization, and dashboard-style financial monitoring that Mint users will find familiar, plus investment tracking and net worth monitoring that Mint never offered.

For users who follow the methodology consistently, yes, YNAB’s own data shows users save an average of $600 in their first two months and $6,000 in their first year, making the $109 annual cost straightforward to justify many times over. The honest caveat is that YNAB’s value is entirely dependent on your willingness to engage with the system regularly. Users who log in weekly consistently report meaningful results, whereas users who check in monthly report minimal impact, regardless of which features they use.

Conclusion

YNAB and Monarch Money are both excellent personal finance tools that fully justify their subscription costs, for the right user. YNAB is the right choice if you need to change your relationship with money, not just track it. The zero-based methodology, four-rule system, 34-day trial, and educational ecosystem make it the strongest tool available for users carrying debt, living paycheck to paycheck, or ready to commit to a structured financial practice that produces measurable behavioral change. Monarch is the right choice if your spending is generally under control and you need a comprehensive, low-friction financial dashboard that shows your complete picture (spending, net worth, investments, and goals) in one place, without requiring daily engagement. The $9 annual price difference between them is irrelevant; the philosophy difference is everything.

The honest recommendation before spending a dollar on either: take YNAB’s 34-day no-credit-card trial and commit to using it properly for one full budget cycle. Therefore, if the active engagement feels sustainable and you notice yourself making more intentional money decisions, YNAB is the app for you. However, if it feels like too much work for the value you’re getting, Monarch’s dashboard approach is likely the better fit for your financial personality, and Monarch’s 7-day trial gives you enough time to confirm that before paying.

Ready to explore more? Visit YourTechCompass for hands-on reviews, buying guides, and how-to articles that cut through the noise and give you exactly what you need.