Picture this. You’re at the checkout counter at a Nairobi supermarket. Your hands are full. Your phone is in your bag. Instead of digging for your card or unlocking your phone to tap Google Pay, you raise your wrist, or your hand, toward the payment terminal, and it’s done. No fumbling. Also, no PIN for low-value transactions. And, no “sorry, my battery is dead.” That’s the experience DTB Wearables is designed to deliver. Launched on April 8, 2026, by Diamond Trust Bank in partnership with Mastercard and powered by Tappy Pay, DTB Wearables represent a genuinely significant moment in Kenya’s payments history; the first time a Tier One bank in the country has brought banking-backed NFC wearable payment devices to market as a formal product line.

This isn’t a fintech experiment or a limited pilot. It’s a real, purchasable product collection, a silicone wristband at KES 1,200, two ring options between KES 2,400 and KES 2,900, orderable through a dedicated catalogue at wearables.diamondtrustbank.co.ke, from one of East Africa’s most established and profitable banks, which posted KES 10.7 billion in profit and grew its customer base by 45% in 2025. This guide is for you; whether you’re a DTB customer curious about whether this product fits your lifestyle, a fintech watcher tracking where Kenya’s cashless journey is heading, an investor evaluating what banking-backed wearables mean for African payments infrastructure, or simply someone who wants to understand the technology before deciding whether to tap in.

What Are DTB Wearables and What Exactly Did DTB Launch?

Before you make any decisions, you need to understand precisely what DTB has brought to market, because the details matter more than the headline.

Diamond Trust Bank is one of East Africa’s most established financial institutions. Founded in 1946 and listed on the Nairobi Securities Exchange, DTB operates across Kenya, Uganda, Tanzania, and Burundi, with a strong retail and SME banking presence built over eight decades. Consequently, when DTB moves into wearable payments, it does so as an institution with regulatory standing, depth of banking licences, and account infrastructure that no fintech startup can replicate from day one.

What DTB launched on April 8, 2026, is a range of NFC-enabled wearable payment devices, linked directly to customers’ existing DTB debit cards, that enable tap-and-pay transactions at any contactless-enabled POS terminal globally. The product was built in collaboration with Mastercard and powered by Tappy Pay, a specialist in wearable payments technology.

Furthermore, DTB’s official product description describes it as enabling “secure, tokenised, and convenient payments through stylish wearable devices.” Three form factors are currently available: a silicone wristband and two ring variants.

The Distinction That Matters Most

DTB Wearables are bank-backed, not prepaid. When you tap a DTB wearable at a terminal, the transaction is drawn directly from your DTB bank account via your linked debit card, not from a separate prepaid wallet that needs to be topped up.

This means the wearable carries the full account depth and regulatory protection of your DTB current or savings account. Additionally, this makes DTB’s product structurally different from prepaid wearable alternatives that fintech startups have historically offered, and from Safaricom’s now-defunct M-Pesa 1Tap wristband, which operated within M-Pesa’s closed merchant network rather than on global card rails.

How DTB Wearables Work: The Technology Explained Simply

NFC stands for Near Field Communication, a short-range wireless technology that operates at 13.56 MHz and allows two devices to communicate when brought within approximately 4cm of each other. It’s the same technology that powers contactless debit cards, Apple Pay, Google Pay, and most modern tap-to-pay terminals. You’ve almost certainly used NFC before without calling it that; every time you’ve tapped your bank card at a Carrefour or Naivas checkout, you’ve used NFC.

What makes the DTB wearable implementation distinctive is passive NFC. The wearable device contains no battery whatsoever.

Power is wirelessly supplied by the NFC reader in the POS terminal, so the wristband or ring requires no charging, power management, or software updates to function for payment. Consequently, it is always on and always ready. The device cannot run out of battery at an inconvenient moment because it doesn’t have one.

The Payment Flow: Step by Step

Here’s exactly what happens when you pay with a DTB wearable:

Step 1

During setup, your DTB wearable is linked to your existing DTB debit card via the Tappy Pay mobile application. You’ll need to download the Tappy Pay app, create an account, and visit a selected DTB branch to complete the activation of the physical device. You can link up to eight DTB wearables to a single account, useful for households or backup devices.

Step 2

At any contactless-enabled POS terminal, such as a supermarket, petrol station, restaurant, or transit point, you bring your wearable within approximately 4cm of the terminal’s NFC reader.

Step 3

The NFC chip in the wearable transmits a cryptographic token, not your actual card number, to the terminal. This tokenisation process is the core security mechanism: each transaction generates a unique encrypted token that is useless to an attacker even if intercepted.

Step 4

The transaction processes through Mastercard’s global payment network, the same network that processes your physical card transactions. The merchant receives payment. Your DTB account is debited. A confirmation is issued.

Step 5

You can view your transaction history in the Tappy Pay mobile app, which shows your last 10 transactions, including the date, amount, and merchant name.

Transaction Limits

The per-transaction limit for DTB Wearables is KES 5,000 per tap, as confirmed in this tweet from the official DTB Kenya X account. The daily limit is KES 10,000. These limits are set at the product level, not the card level, and reflect standard contactless payment risk management.

For transactions above KES 5,000, you’ll need your physical card or another payment method. Consequently, DTB Wearables are optimised for everyday, lower-value purchases (such as groceries, fuel, coffee, and transport), not for large commercial transactions.

The Apple NFC Problem: Why This Actually Matters

Here’s a detail that most coverage of DTB Wearables doesn’t adequately explain. Apple restricts access to the iPhone’s NFC hardware, preventing third-party apps from triggering NFC payments. This means that any tap-to-pay solution in Kenya that relies on a smartphone, including Absa Kenya’s AbsaPay, simply doesn’t work for iPhone users.

iPhone users in Kenya who want tap-to-pay have been stuck because Apple Pay isn’t available in Kenya, and Apple won’t open the NFC hardware to local bank apps. DTB Wearables completely sidestep this problem. Because the NFC hardware is in the wearable device rather than the phone, it works identically whether you’re an iPhone user, an Android user, or a feature phone user.

Your phone is irrelevant to the payment. Furthermore, this is one of the most commercially clever aspects of the DTB Wearables launch; it solves a real pain point for Kenya’s significant iPhone-using population without requiring Apple’s cooperation.

Why DTB Did This: The Strategic Logic Behind the Launch

Understanding why DTB made this move helps you evaluate what it means for the broader market, and whether this is a one-off product launch or the beginning of something larger.

Kenya’s contactless payment volumes have grown significantly since COVID-19 accelerated the adoption of cashless payments. NFC-enabled POS terminals are now widespread in Nairobi’s urban retail environment; supermarkets, petrol stations, hotels, and hospitality outlets all carry contactless-capable hardware.

The infrastructure was ready. The consumer habit was forming. DTB’s move was well-timed to catch that wave before competitors.

Murali Natarajan, Managing Director and CEO of DTB Kenya, described the launch as “a significant step forward in the evolution of digital payments in Kenya, moving beyond traditional cards and devices to deliver secure, always-on payment experiences that fit seamlessly into everyday life.” That language (“always-on”) is deliberate. The pitch is convenience without compromise: a payment credential that is physically inseparable from you by design.

The competitive positioning is equally clear. DTB posted KES 10.7 billion in profit in 2025 and grew its customer base by 45%, a strong year.

Launching a visible, lifestyle-oriented product like payment jewellery is an obvious play for retail visibility among younger, urban customers in Kenya, who have plenty of banking options. The Kenyan banking market is competitive, with KCB, Equity Bank, NCBA, Absa, Co-operative Bank, and Stanbic all competing for the same tech-forward urban customer.

A wearable payment product creates a tangible differentiator that doesn’t fit neatly into a feature comparison chart. Additionally, each wearable creates a persistent, daily-use engagement touchpoint outside mobile banking; every tap is a brand interaction.

The partnership structure is also worth noting. Mastercard provides the global payment network and commercial credibility.

Shehryar Ali, Senior Vice President and Country Manager for East Africa at Mastercard, described the collaboration as “enabling faster, safer transactions and supporting the growth of a truly cashless economy.”

Tappy Pay provides the technical infrastructure, the wearable provisioning, app management, and tokenisation layer. DTB brings the banking licence, the customer base, and the distribution. Consequently, no single party had to build everything from scratch, a smart deployment model that explains how a product of this sophistication reached the market as quickly as it did.

The Three DTB Wearable Devices: Silicone Band, Ceroxy Ring, and Ceramic Ring

Let’s get practical. Here’s exactly what’s available, what each one costs, and who each device is realistically designed for.

Device Comparison Table

Device | Price (KES) | Material | Design Options | Best For | Key Advantage | Honest Limitation |

1,200 | Silicone | Kenya flag | Active, commuters, budget-conscious | Waterproof; most accessible price | Visible on wrist; limited aesthetic options | |

2,400 | Ceroxy composite | Kenya flag or carbon fibre | Professionals, fashion-conscious | Most design options; discrete | Sizing constraints; fit risk | |

2,900 | Ceramic | Kenya flag | Premium users, lifestyle-focused | Scratch-resistant; premium feel | More brittle under direct impact |

The DTB Silicone Band: KES 1,200

The Silicone Band is the most affordable and most accessible form factor. It’s a flexible, waterproof, sweat-resistant wristband in black featuring a Kenyan flag pattern running through it, designed to look like a fitness tracker rather than a banking product.

The Kenya flag design is a deliberate aesthetic choice that makes it feel like a lifestyle accessory rather than a financial tool. It’s the entry point into the DTB Wearables ecosystem, at KES 1,200, it costs less than a restaurant lunch in Westlands.

This is the device for you if you lead an active lifestyle, running, gym sessions, commuting, or any situation where fumbling for a wallet is an inconvenience. It’s also the lowest-risk way to try the product: if you decide wearable payments aren’t for you, you’ve invested KES 1,200 to find that out.

Honest Consideration

Wristbands are the most visible form factor, which means aesthetics matter. Not everyone wants to wear a payment device on their wrist permanently, particularly if it doesn’t complement their style. The current design prioritises national identity over fashion versatility.

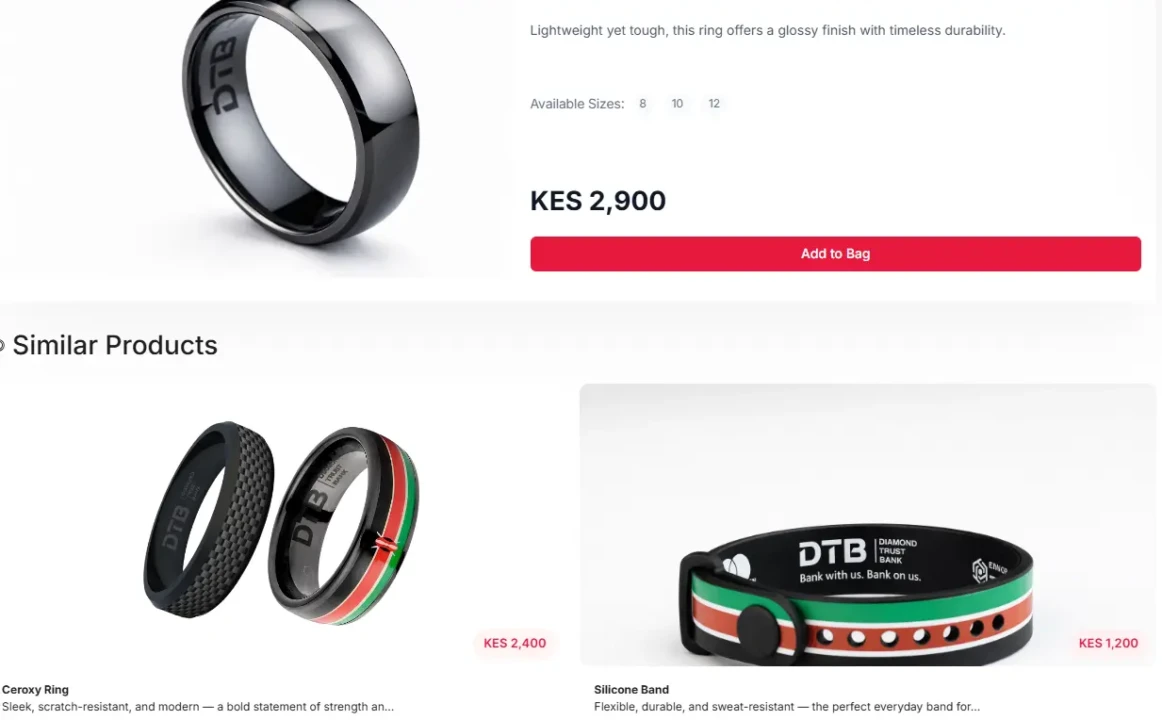

The DTB Ceroxy Ring: KES 2,400

The Ceroxy Ring is the mid-range option, available in two pattern options (Kenyan flag and carbon fibre) and in sizes 8, 10, and 12. Ceroxy is a composite material that balances durability with finish quality.

The ring form factor is the most discreet payment device available in the DTB range. When worn, it is indistinguishable from a regular ring to any observer. Consequently, it’s the choice for professionals, business users, and fashion-conscious consumers who want seamless payment capability without any visible indication that their accessory serves a financial function.

The carbon fibre pattern option is particularly appealing for users who want something that doesn’t reference national identity and fits a wider range of outfits and contexts.

Honest Consideration

Ring sizing is the most significant practical challenge with this form factor. NFC rings must fit correctly to both work reliably and be comfortable to wear all day. DTB offers sizes 8, 10, and 12, a narrower size range than you might find with standard rings. If your ring size falls between these options, fit may be imperfect. Additionally, returns and exchanges for incorrectly sized rings involve more friction than exchanging a wristband.

The DTB Ceramic Ring: KES 2,900

The Ceramic Ring is the premium option in the DTB Wearables collection and is also available in sizes 8, 10, and 12. Ceramic is scratch-resistant, hypoallergenic, and offers a high-end visual and tactile quality, positioning this device closest to fine jewellery. At KES 2,900, it’s the product for users who want their payment wearable to feel like a genuine lifestyle accessory rather than a tech gadget wrapped in fashion.

The scratch resistance of ceramic is a meaningful practical advantage over Ceroxy for everyday use, as rings are knocked against hard surfaces far more often than most people anticipate.

Honest Consideration

Ceramic is durable against scratches but can be more brittle under direct impact. A sharp knock against a hard edge can chip ceramic, whereas it would only scratch Ceroxy. For users who work with their hands in physical environments, this is worth considering.

Setting Up and Using DTB Wearables: A Practical Walkthrough

Here’s exactly what the process looks like from the moment you decide to get a DTB wearable to your first successful payment.

Eligibility and Acquisition

You must be an existing DTB customer with an active DTB current or savings account and a linked DTB debit card. If you’re not a DTB customer, you’ll need to open an account first, which you can do at any DTB branch or through their digital channels.

The wearables are ordered through a dedicated catalogue at wearables.diamondtrustbank.co.ke, DTB’s Wearable Acquisition Portal, where you select your form factor, size (for rings), and complete your order online. Payment for the wearable device itself is made through the portal.

Setup and Activation

After ordering, you need to download the Tappy Pay mobile application and create an account. You’ll then need to visit a selected DTB branch to complete the activation of the physical device. Activation is currently required to link the device to your account.

DTB’s FAQ confirms this: “You will need to visit a selected DTB branch to set up the wearable device.” Consequently, this is a genuine friction point in the onboarding process, particularly for customers who prefer a fully digital setup without a branch visit. It’s worth calling your nearest DTB branch to confirm availability before making a special trip.

Transaction Limits and Daily Use

Once activated, the wearable works at any NFC-enabled POS terminal globally, including supermarkets, petrol stations, restaurants, hotels, and any merchant that accepts Mastercard contactless payments. The per-transaction limit is KES 5,000, with a daily cumulative limit of KES 10,000.

For transactions below KES 5,000, you tap and go. For higher-value purchases, your physical card remains the preferred method. Additionally, your full transaction history is accessible via the Tappy Pay app, including your last 10 transactions, with details such as date, amount, and merchant name.

Security and Loss Management

If your wearable is lost or stolen, contact DTB immediately to deactivate the device. Because the wearable uses tokenisation, transmitting encrypted tokens rather than your actual card number, a lost wearable doesn’t expose your card credentials in the way a lost physical card does.

Furthermore, the limited daily transaction ceiling of KES 10,000 means that even in a worst-case scenario between losing the device and deactivating it, exposure is bounded. Each device also comes with a 12-month warranty from the date of purchase, covering defects and non-functionality.

Maintenance

No charging. No software updates via the wearable itself.

The Tappy Pay app on your phone handles account management, transaction history, and any necessary updates to the linkage configuration. The wearable device’s NFC chip has no battery to replace and no firmware to update; it is a passive component that derives all power from the reader at the point of sale.

DTB Wearables in Kenya’s Cashless Payments Ecosystem

To fully appreciate what DTB has done here, you need to understand the payments landscape it’s entering, and where the wearable fits within it.

Kenya’s payments ecosystem is among the most sophisticated in Africa and the most complex in the world for a market of its income level. M-Pesa, operated by Safaricom, processes over 60 billion transactions annually and has been the dominant payment rail for person-to-person transfers, merchant payments, and bill settlements since 2007.

As our mobile money Africa guide documents in detail, M-Pesa’s penetration of Kenyan financial life is unlike anything else on the continent. It is the default payment method for most Kenyans, from vegetable vendors in Kibera to premium retailers in Karen.

DTB Wearables do not compete with M-Pesa. They operate on an entirely different rail. M-Pesa transactions run on Safaricom’s mobile money network and settle through its own infrastructure.

DTB Wearables run on Mastercard’s global card payment network; the same rail as your DTB debit card. These are parallel systems serving overlapping but distinct use cases. Consequently, a DTB customer’s payment life in Kenya looks something like this: M-Pesa for person-to-person transfers, vendor markets, and matatu fare; DTB Wearables for supermarket checkouts, petrol stations, restaurants, and any NFC-enabled merchant. Furthermore, comparing the two is less useful than recognising that Kenya’s sophistication as a payments market means consumers are increasingly comfortable managing multiple payment tools for different contexts.

The historical context is also important. Safaricom attempted wearable payments in 2017 with M-Pesa 1Tap, a combination of wristbands and NFC stickers piloted in Nakuru. That product is now defunct.

Safaricom shifted its contactless strategy toward smartphone-based tap-to-pay. DTB is picking up the wearable mantle, but with a critical structural difference. The 1Tap wristband only worked within M-Pesa’s closed merchant network.

A DTB wearable works globally at any Mastercard contactless-enabled terminal. That is a vastly larger acceptance network, and it’s why DTB’s version of this product has a meaningfully stronger commercial foundation than Safaricom’s 2017 pilot did.

This also continues a broader pattern in Kenyan banking. In 2024, Absa Kenya launched AbsaPay, enabling Android smartphones to be used as tap-to-pay devices. Banks are systematically removing friction between a customer’s account and the point of sale.

DTB Wearables are the next layer in that progression, not a standalone innovation but a deliberate step in a direction the entire Kenyan banking sector is moving.

For those tracking where digital wallets and contactless payment form factors are heading, our Samsung Wallet vs Google Wallet comparison provides useful context on the structure of the global wearable and digital wallet ecosystem.

Pricing, Fees, and Financial Considerations

Here’s the full picture of what DTB Wearables cost you: device acquisition, ongoing fees, and the financial logic of adopting them.

Device Costs

Silicone Band at KES 1,200, Ceroxy Ring at KES 2,400, Ceramic Ring at KES 2,900. These are one-time purchase costs, not subscription fees. You pay for the device, and it works.

Account Requirements

You must have an active DTB current or savings account with a linked DTB debit card. No special account tiers are required; a standard DTB account qualifies.

Transaction Fees

DTB’s official product page does not explicitly itemise a per-NFC-transaction fee in addition to standard debit card fees. Transactions processed through the wearable are treated as Mastercard contactless debit transactions, meaning they fall under the same fee structure as tapping your physical DTB debit card at a POS terminal. In practice, this means the wearable itself adds no incremental transaction cost beyond what your account already incurs for card payments.

Warranty

Each device carries a 12-month warranty from the date of purchase, covering defects and non-functionality. This provides reasonable protection for a first-generation product during its most likely failure window.

Replacement Costs

DTB’s publicly available documentation does not specify replacement costs for lost, damaged, or post-warranty devices.

Honest Advice: Contact your nearest DTB branch or DTB customer service before purchasing to confirm the replacement policy and associated costs. This information matters particularly for the keychain form factor; a device designed to be attached to everyday keys faces higher exposure to physical damage and loss than a wristband or ring.

The Financial Case for Adoption

If you already have a DTB account and regularly make purchases at NFC-enabled merchants in Nairobi, the silicone band at KES 1,200 is a low-risk entry into the product. You’re not changing your account, your bank, or your transaction habits; you’re adding a more convenient form factor for the card payments you’re already making. The financial case is straightforwardly about convenience, not cost reduction.

What DTB Wearables Mean for African Fintech

A launch like this matters beyond Kenya’s borders, and understanding why requires stepping back from the product to the signal it sends.

Kenya is the most-watched fintech market in Africa. What launches and succeeds here often signals what’s coming across the continent over the next two to five years.

M-Pesa’s Kenyan success inspired mobile money deployments across 40 African countries. AbsaPay’s Android tap-to-pay model will likely roll out to other Absa markets across Africa. DTB Wearables, if it achieves meaningful adoption, could trigger wearable payment launches by KCB, Equity Bank, NCBA, and their regional peers. Furthermore, the Mastercard and Tappy Pay partnership model is replicable by any Tier One bank in Uganda, Tanzania, or Rwanda with a Mastercard issuing relationship that could deploy an equivalent product using the same technology stack.

The truly transformative next version of this product, a mobile money-linked NFC wearable that draws from an M-Pesa wallet rather than a bank account, would be the product that changes financial inclusion at scale. DTB’s launch creates the proof of concept. The inclusion version is the next frontier, and it will likely come from a telco-fintech partnership rather than a traditional bank.

Our AI in Africa coverage tracks a broader convergence happening across this ecosystem: as payment infrastructure like DTB Wearables builds out the physical contactless layer, AI-driven personalised financial services have better data and better delivery mechanisms to operate through. The fintech startups profiled in our African fintech startups to watch article are building on exactly this kind of payment infrastructure.

Honest Limitations and Open Questions

No credible review of a first-generation banking product skips this section.

NFC Terminal Density Outside Nairobi Is the Most Significant Geographic Constraint

The DTB Wearables value proposition depends entirely on contactless-enabled POS terminals being present at the merchants where you shop. In Nairobi’s urban core (Westlands, Karen, the CBD, Kilimani, Lavington), NFC terminal density is high enough to make the wearable genuinely useful on a daily basis.

But, in Mombasa, Kisumu, and Nakuru, coverage is improving but patchier. However, in peri-urban and rural Kenya, NFC infrastructure remains sparse. A payment device you can only use at 30% of your regular merchants is an inconvenience, not a revolution.

Branch Activation Is a Friction Point

The requirement to visit a DTB branch to complete wearable setup is a genuine barrier in 2026, when consumers expect fully digital onboarding for financial products. It’s understandable from a security and KYC perspective, but it will slow adoption among users who are not already regular branch visitors.

The M-Pesa Ecosystem Gap Remains

Kenya’s dominant payment behaviour is M-Pesa. Until NFC wearables can trigger M-Pesa payments directly (operating on the mobile money rail rather than the card rail), they operate in a parallel ecosystem that excludes the payment behaviour most deeply embedded in Kenyan consumer life.

This is not a DTB-specific failure; it’s a structural reality of the two payment systems’ architecture. But it means DTB Wearables complement your payment life rather than simplifying it into one tool.

Consumer Education Investment Is Substantial

Wearable payments are genuinely new to most Kenyan consumers. The concept of tapping a ring at a checkout terminal to pay is not self-explanatory; it requires a behaviour change that even contactless cards took years to normalise. DTB and Mastercard will need sustained investment in consumer education to drive meaningful adoption beyond early-adopter urban professionals.

First-Generation Product Reality

DTB Wearables is a first-generation product. As with any first-generation payment hardware, there will likely be software updates, compatibility refinements with specific POS configurations, and UX improvements needed before the product feels as seamless as a mature payment platform. Consequently, early adopters should expect occasional friction and should engage DTB customer service when they encounter it.

Your feedback directly shapes the product’s evolution.

FAQs

You can use DTB Wearables at any contactless-enabled POS terminal that accepts Mastercard, such as supermarkets, petrol stations, hotels, restaurants, and most modern retail environments in Nairobi and other major Kenyan cities. The wearables are also compatible with Mastercard contactless terminals globally, meaning they work when you travel internationally. The per-transaction limit is KES 5,000, and the daily limit is KES 10,000.

Yes. DTB Wearables uses tokenisation, which means your actual card number is never transmitted during a transaction. Each payment generates a unique encrypted token that cannot be reused or exploited even if intercepted. Additionally, the daily transaction ceiling of KES 10,000 limits financial exposure in the event of loss. If your wearable is lost or stolen, contact DTB customer service immediately to deactivate the device and prevent further transactions.

The Silicone Band costs KES 1,200. The Ceroxy Ring costs KES 2,400 and is available in sizes 8, 10, and 12, in Kenya flag or carbon fibre designs. The Ceramic Ring costs KES 2,900 and is also available in sizes 8, 10, and 12. These are one-time device purchase prices; there is no subscription fee. Devices come with a 12-month warranty covering defects and non-functionality. Orders are placed through DTB’s dedicated wearable portal at wearables.diamondtrustbank.co.ke.

Yes, unconditionally. You must have an active DTB current or savings account with a linked DTB debit card. DTB Wearables link to your existing debit card and allow you to draw from your DTB account balance. You cannot use a wearable with another bank’s account. If you want the product and don’t have a DTB account, you’ll need to open one. Up to eight wearables can be linked to a single DTB account, useful for household members sharing an account or for maintaining multiple form factors.

They operate on entirely different payment rails serving overlapping but distinct use cases. M-Pesa runs on Safaricom’s mobile money network, used for person-to-person transfers, paybill payments, and by merchants with M-Pesa tills. DTB Wearables run on Mastercard’s global card network and are accepted at any NFC-enabled contactless terminal that accepts card payments. A wearable cannot send money to another person’s M-Pesa number. An M-Pesa payment cannot be tapped at a Mastercard contactless terminal. They are complementary tools, not substitutes for each other.

Conclusion

DTB Wearables represent a genuinely consequential moment in Kenya’s cashless payments journey, and a clever, strategically timed product from a bank that understood exactly the gap it was filling. The Apple NFC problem is real, and DTB’s wearable elegantly solves it. The product works globally, carries Mastercard’s acceptance network, costs less than most Kenyans spend on a restaurant meal (at the entry level), and creates a payment credential that is literally inseparable from you by design. Furthermore, the Mastercard and Tappy Pay partnership means DTB built this on proven global wearable payment infrastructure rather than engineering from scratch, which should translate into reliability and scalability that first-generation banking experiments sometimes lack. For Kenya’s urban, formally banked, iPhone-owning, or Android-carrying professional, this product solves a real problem in a convenient, affordable way.

The honest limitations are equally worth naming. Branch activation adds friction. NFC terminal density outside Nairobi’s urban core constrains the value proposition. The M-Pesa rail gap means this product serves one slice of Kenya’s payment behaviour, not all of it. And as a first-generation product, you should expect a learning curve for both you and DTB. But none of those limitations diminishes what DTB has demonstrated: that Kenya’s established banks are willing and capable of leading payment hardware innovation, not just following fintech startups into new territory. If the wearable payments category takes hold here, and the fundamentals suggest it might, DTB will be remembered as the institution that first proved it was possible with banking infrastructure behind it.

Kenya’s payments story is one of the most important technology narratives on the continent, and it’s moving fast. Head to YourTechCompass.com to stay current on the African fintech and tech innovations that are reshaping how money moves across East Africa and beyond.