Nigeria’s digital lenders disbursed $865 million in loans in 2025, according to the Central Bank of Nigeria’s Fintech Report 2026, with annualized transaction growth exceeding 45% since 2022. That number represents millions of individual Nigerians accessing credit that traditional banks consistently refused them, often within minutes of applying, with nothing more than a smartphone and a BVN. Digital lending in Nigeria is one of the most consequential financial developments in the country’s recent history, and one of the most misunderstood. By mid-2025, over 1,500 loan apps were available to Nigerian users, yet fewer than 300 had official approval from either the CBN or the FCCPC. The gap between those two numbers tells you almost everything you need to know about why this space demands careful attention.

This guide is for you, whether you’re a first-time borrower evaluating which loan app to trust, a small business owner looking for working capital, a remote worker comparing digital credit options, or a fintech watcher tracking where Nigeria’s lending ecosystem is heading. What follows is a researched, honest, and detailed breakdown of how digital lending works in Nigeria, who the key players are, what it actually costs, what your rights are, and how to protect yourself in a market that has produced both genuine financial inclusion and documented borrower abuse. No promotions. No affiliate links. Just the full picture.

Why Digital Lending Took Off in Nigeria

To understand digital lending in Nigeria, you need to start with the problem it was built to solve. Less than 4% of Nigerian adults had access to formal credit before mobile lending arrived at scale, a figure that reflects not just poverty, but the structural exclusion built into traditional banking.

Banks required collateral, guarantors, formal employment documentation, and credit histories that most Nigerians simply didn’t have. Consequently, over 40 million Nigerian adults remained excluded from formal financial services even as Nigeria’s economy grew. SMEs, which form the backbone of Nigeria’s informal economy and account for roughly 80% of employment, were routinely denied credit by institutions that had no framework for assessing their risk.

Digital lending changed the equation by changing the data. Rather than requiring a salary slip or a land title, digital lenders could assess creditworthiness using the phone in your pocket, airtime top-up frequency, mobile transaction history, location consistency, app usage patterns, and BVN-linked financial behavior.

The BVN (Bank Verification Number), introduced by the CBN in 2015, provided digital lenders with a unified digital identity anchor, enabling remote verification at scale. Furthermore, the explosive growth of mobile penetration (Nigeria now has over 180 million SIM subscriptions), combined with smartphone expansion and fintech infrastructure from platforms like Paystack, Flutterwave, and Mono, provided the payment rails and open banking data layers that digital lending required to function.

The Outcome

The result was a leapfrog: Nigeria built a functional credit market for previously excluded populations without needing the physical infrastructure (branches, credit bureaus, collateral registries) that credit markets in developed economies depend on. Digital lending platforms now account for over 40% of microloan disbursements in Nigeria’s urban regions, according to EFInA data.

Moreover, by August 2025, the number of approved digital lenders had surged 166% to 461, up from 173 in April 2023. That growth trajectory tells you this was not a niche experiment. It became a core pillar of Nigeria’s financial inclusion story, and as you’ll see, both its best and worst chapters are still being written.

How Digital Lending Works in Nigeria

Here’s what the borrowing process actually looks like, from the moment you open an app to the moment funds hit your account. Understanding each step makes you a smarter, more protected borrower.

Step 1: Registration

You download the loan app and register using your phone number and BVN. Your BVN is the key that unlocks your identity across Nigeria’s banking system; it connects your loan application to your bank transaction history, existing loans, and repayment record.

Additionally, most apps will require you to link a bank account for disbursement and repayment. Some require a government-issued ID for higher loan amounts.

Step 2: Permissions

This is the step most borrowers rush through, and it’s where the biggest privacy risks live. Most digital lending apps request access to your contacts, SMS history, transaction data, and sometimes photos, location, and microphone.

The honest truth is this: under Nigeria’s DEON Consumer Lending Regulations, enacted in July 2025, lenders are prohibited from accessing a borrower’s contacts, photos, or private messages. Granting contact access is not a legal requirement. Consequently, any app that makes contact access mandatory as a condition of borrowing violates current FCCPC rules.

Read every permission request carefully before tapping “Allow.”

Step 3: AI Credit Scoring

Once registered, the platform’s machine learning algorithms assess your creditworthiness in real time. These algorithms rely on non-traditional digital data mined from your mobile phone (airtime purchase patterns, transaction frequency, spending behavior, and social graph signals) alongside any available credit bureau data for repeat borrowers. This happens within seconds to minutes. Furthermore, credit bureau data from providers like First Central is increasingly integrated into subsequent lending decisions, meaning your repayment behavior on one platform affects your access to credit on others.

Step 4: Loan Offer

Based on the credit assessment, the platform generates a loan offer, specifying the principal amount, tenure (typically 7–180 days), interest rate, and total repayment amount. First-time borrowers typically access smaller amounts at higher rates.

Established customers with good repayment history unlock larger amounts at lower rates. The rate you’re offered isn’t fixed; it varies based on your credit profile and loan size.

Step 5: Disbursement

Once you accept the offer, funds are typically disbursed to your linked bank account within minutes to a few hours. This speed is one of digital lending’s most genuine advantages over traditional banking; an institution that takes weeks to approve a loan simply cannot serve someone who needs ₦30,000 for a medical bill today.

Step 6: Repayment

Repayment is typically via direct debit from your linked bank account on the due date. Many platforms also allow manual transfer or payment via USSD.

Missing a payment triggers late fees and, critically, negative reporting to credit bureaus. Moreover, the CBN’s Global Standing Instruction (GSI) allows lenders to recover unpaid loans from any bank account linked to your BVN, meaning a default with one digital lender can result in funds being recovered from your account at a completely different bank.

The Digital Lending Landscape in Nigeria: Key Players

Nigeria’s digital lending ecosystem spans consumer credit, SME lending, and embedded finance. Here’s a grounded look at the key platforms operating in 2026, with honest assessments of each.

Carbon (Formerly Paylater)

Carbon is one of Nigeria’s oldest digital lenders, having launched in 2016 as Paylater and later evolving into a full digital bank and lending platform. In 2024, Carbon acquired Vella Finance through its parent company, One Credit Limited, expanding its product suite into business banking.

It offers personal loans, savings, investments, and bill payments. Carbon operates as a CBN-licensed microfinance bank, subject to stricter oversight and to deposit insurance coverage up to ₦500,000. Furthermore, as one of the platforms that helped establish the credibility of Nigerian digital lending, Carbon’s repayment rates and underwriting standards are among the most mature in the sector.

Honest Limitation: Carbon’s loan limits for first-time borrowers are conservative. Therefore, you won’t be able to access large amounts immediately, and rate offers for new users can be higher than those for more established alternatives.

FairMoney

FairMoney has grown into one of Nigeria’s largest digital banking platforms, serving over 10 million users with instant loans, savings accounts, and bill payments. It operates as a CBN-licensed microfinance bank and has raised a Series C round backed by international investors.

FairMoney’s credit model scores borrowers based on mobile transaction data and behavioral signals, offering loan tenures ranging from 1 to 18 months. Consequently, it’s one of the more versatile lenders in terms of product range and ticket size.

Honest Limitation: FairMoney’s interest rates can be high for short-term, small-amount loans. Its digital bank positioning makes the product more complex than pure loan apps, a feature for experienced users and a source of friction for first-timers.

Branch

Branch is a US-backed digital lender operating in Nigeria with structured compliance, credit reporting, and borrower protection measures built in from its founding. It uses machine-learning models trained on mobile phone data to assess creditworthiness and consistently ranks among the most transparent platforms for fee disclosure. Moreover, Branch integrates with credit bureaus for both assessment and reporting, meaning successful repayment improves your credit profile across the ecosystem.

Honest Limitation: Branch’s initial loan offers are typically small, and the approval process can be slower than pure instant-approval apps. However, the trade-off is lower rates and better regulatory compliance.

Renmoney

Renmoney operates as a CBN-licensed finance company, one of the clearest examples of a traditional regulatory structure applied to a digital lending product. It serves both consumers and small businesses, offering loan tenures up to 24 months for larger amounts. CBN licensing means that Renmoney undergoes regular audits, maintains minimum capital requirements, complies with banking regulations, and has formal dispute-resolution mechanisms.

Honest Limitation: Renmoney’s documentation requirements are more extensive than those of pure app-based lenders, reflecting its regulatory obligations rather than unnecessary friction.

PalmCredit

PalmCredit offers instant personal loans with no collateral, minimal documentation, and quick disbursement, making it popular for small-ticket, urgent borrowing needs. It operates under FCCPC registration and is one of the more widely used consumer lending apps in Nigeria’s mass market.

Honest Limitation: PalmCredit’s interest rates are on the higher end of the consumer lending spectrum, and its loan limits are low for new users. It is best suited for genuinely small, short-term needs, not medium-term financing.

Moniepoint

Moniepoint is Nigeria’s fastest-growing business banking platform, serving over 10 million customers and processing over $250 billion in annual transactions. It extends working capital loans to SMEs based on their transaction history through Moniepoint’s POS and banking ecosystem.

Additionally, Moniepoint’s SME lending model is one of the most commercially validated in the space, using actual business revenue data rather than proxy behavioral signals to underwrite credit. Its international expansion into Kenya and the UK further signals institutional maturity.

Honest Limitation: Moniepoint’s lending is primarily accessible to businesses actively using its banking and POS infrastructure; it’s not a general-purpose consumer loan product.

Lidya

Lidya focuses on SME credit scoring and lending, targeting small businesses underserved by both traditional banks and consumer-focused digital lenders. It uses a proprietary credit scoring model to assess business financial health and extend credit to businesses that would otherwise have no access to working capital. Furthermore, Lidya has been backed by international investors and development finance institutions who view Nigeria’s SME credit gap as one of the continent’s most important financing opportunities.

Honest Limitation: Lidya’s onboarding requires more documentation than consumer apps, and its loan products are not designed for personal borrowing needs.

Digital Lending Platform Comparison

Platform | Type | Loan Range | Target User | CBN/FCCPC Status | Notable Feature |

Carbon | Consumer + Digital Bank | ₦1,500–₦3M | Individuals | CBN-licensed MFB | Longest track record; full banking suite |

FairMoney | Consumer + Digital Bank | ₦1,500–₦5M | Individuals | CBN-licensed MFB | 10M+ users; 18-month max tenure |

Branch | Consumer | ₦1,000–₦500K | Individuals | FCCPC registered | Strong credit bureau integration |

Renmoney | Consumer + SME | ₦6,000–₦6M | Individuals + small businesses | CBN-licensed Finance Company | Up to 24-month tenure |

PalmCredit | Consumer | ₦2,000–₦300K | Mass market individuals | FCCPC registered | Fastest approval; no documentation |

Moniepoint | SME | Varies by business | Business owners | CBN-licensed MFB | Transaction-based underwriting |

Lidya | SME | ₦150K–₦150M | Small businesses | FCCPC registered | Institutional-grade SME credit scoring |

Interest Rates, Fees, and the True Cost of Digital Loans

This is the section where you need to slow down and read carefully, because the advertised rate and the actual cost of a digital loan in Nigeria often differ significantly.

How Rates Work in Practice

CBN-licensed microfinance banks like FairMoney and Renmoney offer monthly rates of 2.5–8%, making them the most affordable digital lenders. Pure digital lenders range from 5% to 15% per month. For short-term consumer loans (30 days or less), rates can reach 10–15% per month, which annualizes to 120–180% APR or higher.

First-time borrowers with limited credit history pay the highest rates, typically 10–15% monthly. However, established customers with perfect repayment history access rates of 3–5% monthly from the same lender. Furthermore, smaller loan amounts face higher rates because fixed processing costs represent a larger percentage of the principal.

The Hidden Fees

The explicit interest rate is only one component of your total cost. Most platforms also charge processing fees, credit check fees (ranging from ₦70 to ₦1,500 per application), and insurance fees bundled into the loan. Late-payment penalties apply if you miss a repayment date, and they can be significant. Consequently, the total repayment amount is always higher than the stated principal plus stated interest rate.

A Real-World Calculation

Here’s exactly what a ₦50,000 loan over 30 days looks like at a 10% monthly rate with a 2% processing fee:

- Loan principal: ₦50,000

- Processing fee (2%): ₦1,000 deducted upfront (you receive ₦49,000)

- Monthly interest (10%): ₦5,000

- Total repayment due: ₦55,000

- Effective cost on amount received: 12.2% for 30 days

- Annualized Percentage Rate: approximately 146%

That’s not an extreme example; it’s representative of the mid-market for consumer digital loans in Nigeria. Additionally, if you miss the repayment date, late fees accumulate, the APR increases further, and the platform reports the default to credit bureaus. The debt trap dynamic (taking a second loan to repay the first) begins exactly here.

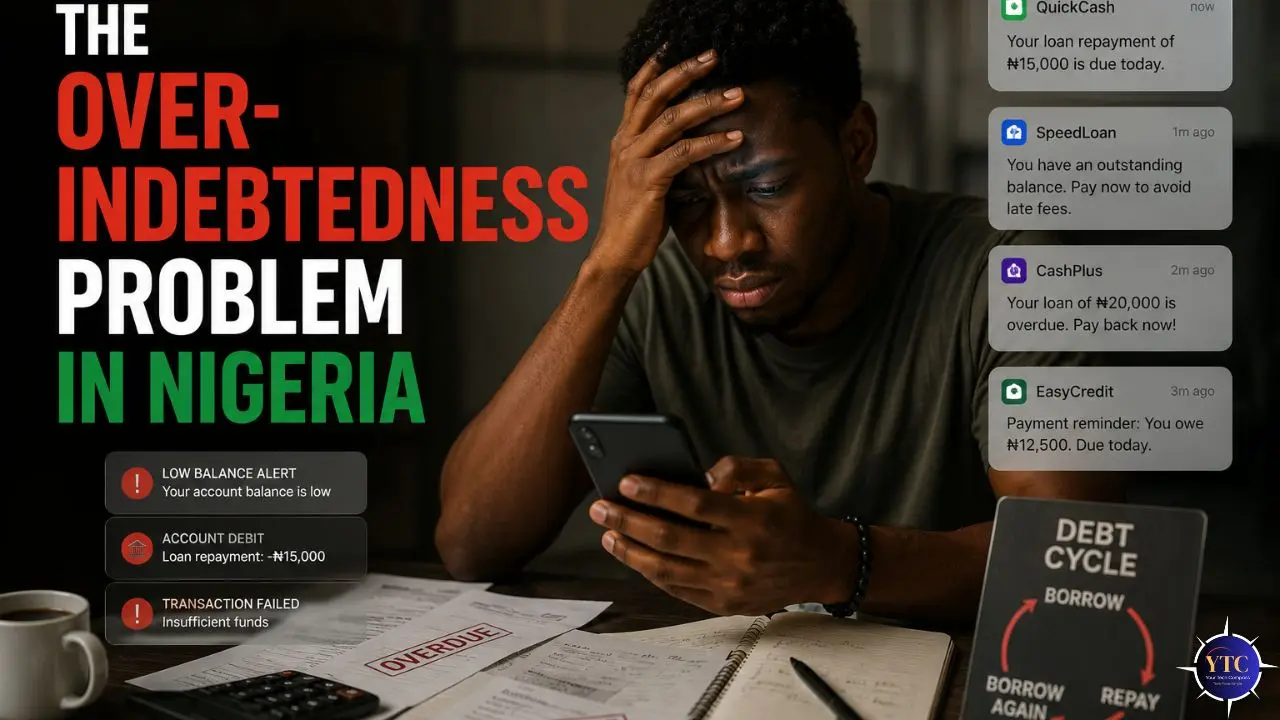

The Over-Indebtedness Problem

By January 2025, retail loans in Nigeria had surged 92.2% to ₦1.73 trillion, reflecting what analysts described as desperate survival borrowing rather than productive economic activity, driven by food inflation that had soared above 40% in late 2024. When millions of Nigerians borrowed to pay for rice and rent, default rates climbed throughout early 2025.

The CBN’s Q2 2025 Credit Condition Survey reported rising default rates across both secured and unsecured lending. The honest advice: a digital loan designed for a 30-day emergency should not become a 6-month cycle of refinancing. Always calculate the total repayment amount before accepting any offer, not just the stated interest rate.

CBN and FCCPC Regulation of Digital Lending in Nigeria

Nigeria’s regulatory journey on digital lending is a story of rapid growth, followed by documented harm, followed by a meaningful, if still incomplete, regulatory response. Understanding where the rules stand in 2026 directly affects how you should evaluate any platform you’re considering.

The Regulatory Timeline

The early period from 2016 to 2020 was largely ungoverned. Digital lenders entered a regulatory vacuum and grew explosively, with some platforms engaging in practices (contact list shaming, intimidation, illegal data access) that were predatory by any reasonable definition.

In 2022, the FCCPC introduced its Limited Interim Regulatory/Registration Framework and Guidelines for Digital Lending, requiring all digital lenders to register. The joint FCCPC/CBN enforcement action that followed removed over 47 apps from the Google Play Store.

The most significant development came in July 2025 with the enactment of the DEON Regulations; the Digital, Electronic, Online and Non-Traditional Consumer Lending Regulations, which replaced the 2022 interim guidelines with a comprehensive, enforceable framework. Mandatory FCCPC registration is now required for every digital lender, with an application fee of ₦100,000 and an approval fee of ₦1,000,000 for up to two mobile applications.

Strict data privacy requirements mandate compliance with the Nigeria Data Protection Act (NDPA) 2023. Ethical debt recovery standards strictly forbid defamatory messages or shaming tactics. Furthermore, the FCCPC set a January 2026 compliance deadline for digital lenders, with a final grace period extended to April 2026, after which non-compliant platforms will be removed from app stores and may face prosecution.

In 2026, over 430 lenders have been authorized, and as of February 2026, 457 companies hold full FCCPC approval, 35 have conditional approval, and 103 are under watch. Additionally, the CBN unveiled an 18-month fintech roadmap in February 2026 focused on implementing open banking, strengthening supervision, and enabling secure cross-border interoperability, a defining step toward the next phase of digital lending infrastructure.

How to Verify a Lender is Legitimate

Check the FCCPC’s Database of Approved Digital Money Lenders at fccpc.gov.ng, which is updated monthly. Legitimate apps must display an “FCCPC Certified” badge and provide a verifiable Nigerian office address.

The CBN regulates microfinance banks and commercial banks offering loans; platforms like FairMoney, Carbon, Renmoney, and Aella, which operate as CBN-licensed microfinance banks, are subject to stricter oversight, deposit insurance, and formal dispute-resolution mechanisms.

Consequently, before borrowing from any platform, spend two minutes verifying its registration status. That check could protect you from significant financial and emotional harm.

The Dark Side: Predatory Lending and Borrower Abuse

This section exists because any honest guide to digital lending in Nigeria must clearly name what went wrong (and what still goes wrong) without softening the truth.

Contact List Shaming

The most documented form of abuse in Nigerian digital lending is contact list shaming: when a borrower misses a payment, the lender’s system automatically sends messages to everyone in the borrower’s contacts, including family, colleagues, employers, and friends, disclosing the debt in language designed to humiliate. This practice caused documented psychological harm across thousands of Nigerian borrowers.

It is not an edge case. It was widespread, systematic, and deliberate on some platforms. The DEON Regulations of 2025 explicitly prohibit this practice. In 2025, the FCCPC introduced fines of ₦50 million to ₦100 million, or 1% of annual turnover, for lenders who engage in unethical conduct or violations. However, enforcement against platforms operating through unofficial download channels remains incomplete.

Unauthorized Data Access

Apps accessing photos, messages, location history, and microphone data beyond what is declared in their privacy policies have been documented in Nigerian digital lending. Some platforms registered as technology or data-processing companies rather than financial institutions specifically to avoid financial regulation while still controlling key lending decisions.

This regulatory arbitrage allowed them to access sensitive user data under technology company permissions while acting as lenders without lending oversight. Furthermore, the NDPA 2023 and DEON Regulations now prohibit accessing a borrower’s contacts, photos, or private messages, but compliance remains enforced across hundreds of active platforms.

The Debt Trap and Mental Health Consequences

The combination of high rates, short tenures, and aggressive collection created a documented cycle of over-indebtedness. Borrowers who couldn’t repay within 30 days took out second loans from other platforms to repay the first, a pattern that compounds costs and risk.

Documented cases of psychological distress and reported suicides linked to predatory digital lending practices have been cited in Nigerian media and policy discussions. This is not a fringe issue.

It reflects what happens when credit becomes accessible to vulnerable populations without adequate consumer protection infrastructure. The honest framing for you as a borrower is this: borrow only what you can repay with certainty on the due date.

Your Rights as a Digital Borrower in Nigeria

Nigeria’s regulatory framework now provides you with genuine, enforceable protections. Here’s what you need to know before and after you borrow.

Right to Full Disclosure

Under the DEON Regulations, all interest rates and hidden fees must be disclosed before you accept a loan. A lender that cannot or will not tell you the total repayment amount before you confirm is in violation of current law. Evasiveness or pressure to “just accept” is a red flag, not a negotiating tactic.

Right to Refuse Contact Access

Any app that makes access to the contact list a mandatory condition for borrowing is in violation of FCCPC guidelines. You have the right to refuse this permission. If the app blocks your application as a result, that tells you something important about how the platform intends to operate if you fall behind on repayment.

Right to Report Harassment

If a digital lender contacts your family, colleagues, or friends about your debt, or sends threatening, defamatory, or humiliating messages, you can report this directly to the FCCPC at fccpc.gov.ng. You can also report to the CBN’s Consumer Protection Department for lenders operating under CBN licensing. Additionally, you can contest unfair debt collection practices through the formal consumer protection framework.

Credit Bureau Reporting

Digital lenders report to Nigeria’s credit bureaus, including First Central and CreditRegistry. Defaults affect your ability to borrow from any regulated institution in Nigeria. Conversely, consistent repayment builds a credit profile that unlocks better rates and higher limits over time. Treat your digital loan repayment as a credit-building exercise, not just a transaction.

Your Pre-Borrowing Checklist

Before accepting any digital loan in Nigeria, ask yourself these questions. Is the platform on the FCCPC’s approved DML list? What is the exact total repayment amount, not just the rate? Also, what permissions does the app request, and are they proportionate to a lending service? And, what is the late payment penalty? Does the platform report to credit bureaus? If you can’t answer all five with confidence, don’t confirm the loan.

Digital Lending vs Traditional Bank Loans: The Honest Comparison

Digital loans are not better or worse than traditional bank loans in any absolute sense. They are appropriate for different situations. Here’s the honest head-to-head.

Feature | Digital Lending | Traditional Bank Loan |

Approval Speed | Minutes to hours | Days to weeks |

Collateral Required | No | Often yes |

Documentation | Minimal (BVN, phone) | Extensive (payslips, guarantors) |

Loan Amounts | ₦1,000–₦5M (most platforms) | ₦500,000+ typically |

Monthly Interest Rate | 2.5–15% monthly | 1–3% monthly |

Credit Scoring Method | AI/mobile data | Formal credit history + documentation |

Accessibility | Anyone with a smartphone + BVN | Formally employed or banked |

Regulation | Improving; DEON enforced from 2025 | Tightly regulated by CBN |

Recourse If a Dispute Arises | FCCPC complaint | Banking ombudsman + CBN |

Deposit Insurance (Savings) | Only CBN-licensed MFBs | Yes, via NDIC |

When digital lending makes sense: small amounts, genuine urgency, no collateral available, and where the total repayment cost is affordable within your cash flow. When it doesn’t: large amounts, medium-term financing needs, or when the monthly rate makes the total repayment unsustainable. Consequently, the smartest approach is to use digital loans surgically (for specific, short-term needs with a clear repayment plan) rather than as a default source of credit.

The Future of Digital Lending in Nigeria

Several forces are converging to reshape digital lending in Nigeria over the next two to three years, and understanding them helps you make smarter borrowing decisions today.

Open Banking

This is the most consequential structural change coming. The CBN’s open banking framework began limited commercial operations in 2026, allowing licensed participants to share customer-consented data securely through standardized APIs.

Early applications focus on payment initiation and on improving credit scoring for SMEs and informal-sector individuals. Consequently, with better access to verified financial data, lenders will be able to refine underwriting models and develop more tailored, fairer products, reducing the reliance on proxy behavioral signals that drive current high rates for first-time borrowers.

Embedded Lending

Embedded lending is already arriving. Financial services are increasingly being integrated into non-financial platforms, such as ride-hailing apps, online marketplaces, utility payment systems, and agritech platforms. Micro-loans appearing natively inside the platforms where Nigerians already transact represent the next phase of digital credit distribution. Furthermore, platforms like Moniepoint, which underwrite SME credit based on actual business transaction data rather than proxies, are demonstrating what embedded lending looks like at scale.

Consolidation Is Inevitable

The number of approved digital lenders surged 166%, from 175 to 461, by August 2025. That crowding, combined with tightening compliance requirements under DEON and the high cost of regulatory spending (estimated at 7% of operating costs for digital lenders in 2025), will squeeze smaller, less-capitalized platforms. The industry is moving from growth-at-any-cost to sustainable, compliant operations, and the lenders that survive that transition will be meaningfully more trustworthy than many operating today.

For a broader understanding of how Africa’s fintech ecosystem is evolving, including the platforms building the infrastructure beneath digital lending, explore our African fintech category hub. Additionally, our African fintech startups to watch article covers the key players reshaping credit, payments, and banking across the continent. Also, for the full context of mobile money and fintech in Africa, our mobile money Africa guide provides essential background on the infrastructure that digital lending in Nigeria depends on.

FAQs

Verify any platform against the FCCPC’s Database of Approved Digital Money Lenders at fccpc.gov.ng, updated monthly. As of February 2026, 457 companies hold full FCCPC approval, 35 have conditional approval, and 103 are under watch. Platforms like Carbon, FairMoney, Renmoney, Branch, and Moniepoint are among the most trusted because they combine FCCPC registration with CBN-licensed microfinance bank status, the highest available regulatory standard.

Under Nigeria’s DEON Consumer Lending Regulations, enacted in July 2025, lenders are prohibited from accessing a borrower’s contacts, photos, or private messages. You have the right to refuse access to contact. Any app that makes contact access mandatory as a condition of borrowing violates current FCCPC rules. If an app is blocked when you decline, that is critical information about how it operates.

Report directly to the FCCPC at fccpc.gov.ng using the consumer complaint portal. For platforms operating as CBN-licensed microfinance banks, you can also report to the CBN’s Consumer Protection Department. Document every harassment message; screenshot, save, and timestamp them before filing. In 2025, the FCCPC introduced fines ranging from ₦50 million to ₦100 million for lenders engaging in unethical conduct. Your report contributes to enforcement.

It depends on the platform and your credit profile. Consumer platforms typically range from ₦1,000 to ₦5 million. Renmoney offers up to ₦6 million for qualified borrowers. Moniepoint’s SME lending goes significantly higher for established businesses with transaction history. First-time borrowers typically start at the lower end of each platform’s range, typically ₦1,000 to ₦50,000, and unlock higher limits by making consistent repayments.

Conclusion

Digital lending in Nigeria is one of the most powerful financial inclusion tools the country has ever deployed, and it has caused documented harm to real people when operating without adequate guardrails. Both statements are true simultaneously, and holding both is the only honest way to evaluate the space. The $865 million disbursed in 2025 represents millions of Nigerians accessing credit that traditional banks refused them, funding school fees, medical bills, small business stock, and survival needs during a period of acute economic pressure. That is a genuine achievement. Furthermore, the DEON Regulations enacted in July 2025, combined with FCCPC enforcement and the CBN’s open banking roadmap, represent a serious and improving institutional response to the abuses of the early years.

What this means for you today is specific and practical. The protections available to you as a Nigerian digital borrower in 2026 are meaningfully stronger than they were two years ago, but the responsibility to use them starts before you borrow, not after a problem occurs. Verify the platform. Calculate the total repayment amount. Refuse unnecessary permissions. Borrow only what you can repay on the due date. And if something goes wrong, report it, because enforcement only improves when borrowers use the mechanisms built to protect them. Additionally, as open banking matures and consolidation reshapes the lender landscape, the digital credit market available to you in two years will be more trustworthy, better priced, and more fairly regulated than it is today. Get informed now, so you’re positioned to benefit when it does.

There’s a lot more to explore across Africa’s evolving fintech and digital credit landscape. Head over to YourTechCompass.com for in-depth guides, platform comparisons, and practical tools that help you navigate digital finance with confidence.