Picture this: a Kenyan software company wins a contract with a Nigerian client. The work is done. The invoice is sent. What happens next is the problem. To get paid, that payment will likely route from a Lagos bank through a US correspondent bank in New York, convert from naira to dollars, cross back across the Atlantic, convert again from dollars to Kenyan shillings, and arrive three to five business days later; minus anywhere from 7% to 12% in fees and FX spreads. Two African businesses, separated by a four-hour flight, paying more to transact with each other than they would to transact with a counterpart in London or New York. A Ghanaian importer settling an invoice with a Senegalese supplier, a South African logistics firm collecting payments across five African countries, an Ethiopian manufacturer paying a Ugandan raw materials supplier; every one of these scenarios carries the same fundamental dysfunction: moving money across African borders is absurdly expensive and slow relative to the geographic and economic proximity of the parties involved.

The root of this dysfunction is structural, not accidental. Intra-Africa trade remains a relatively small share of total African trade, far below the levels seen in Europe and Asia, and weak cross-border payment infrastructure is a key reason. Africa’s trade landscape is fragmented across many currencies and regulatory regimes, and until recently it lacked widely adopted continental settlement infrastructure for commercial payments. The AfCFTA, now ratified by 47 countries, reflects the policy intent to close that gap. The World Bank estimates the agreement could lift income by about 7 percent, or roughly $450 billion, by 2035. But that outcome depends on functional cross-border payment rails, which are now being built piece by piece across institutional and commercial layers. This guide covers what that infrastructure looks like in 2026: the PAPSS institutional layer; the commercial gateways businesses can use today; where corridor coverage is strong and where it still breaks down; and how founders, CFOs, and operations leads can make payment decisions now while the stack is still maturing.

Why Intra-Africa Payments Are So Expensive: The Root Causes

Before the solutions make sense, the specific structural problems behind them need to be understood clearly, because the reason a given gateway or solution works in one corridor and fails in another almost always traces back to one of these underlying causes.

The Correspondent Banking Problem

The core issue is structural. Many intra-African transactions still rely on correspondent banking networks routed through financial centers such as New York, London, or Paris, not because African banks lack the intent to connect directly, but because the inter-bank settlement infrastructure for African trade has long been incomplete. The result is slower settlement, additional intermediaries, and higher costs than the geography would suggest are necessary.

The World Bank’s remittance data show that global remittance costs were about 6.49% in early 2025, while Sub-Saharan Africa remained the most expensive region, at roughly 8.45%-8.78%, well above the UN’s 3% target. In some corridors, especially those involving restricted-currency markets, total costs can rise further once FX spreads and correspondent fees are included. PAPSS has been positioned as a major cost-saving layer for the continent, with estimates that it could save billions annually by reducing reliance on offshore routing and repeated currency conversion.

The Mechanics Make the Cost Visible

A Ghanaian cedi payment to a Nigerian naira account may pass through multiple correspondent banks and currency conversions before it settles; for instance, it converts cedi to USD at the sender’s correspondent, routes through New York, converts USD to naira at the receiver’s correspondent in London or New York, then settles in Lagos. Each intermediary can take a margin; FX is often converted more than once, and settlement can take several business days rather than the near-instant transfer both sides would prefer for working-capital management.

The 54-Currency Problem

Africa has more than 50 currencies, and several of them are not freely convertible in practice. The Nigerian naira, Ghanaian cedi, Ethiopian birr, Sudanese pound, and others can face restrictions or scarcity, which push businesses to route payments through hard-currency intermediaries. Even when two African companies want to trade in their own currencies, the direct infrastructure often does not exist, so they invoice in USD, take on FX risk, and tie up working capital in dollar liquidity.

The practical consequence for B2B trade is significant. Companies that hold local currency may still struggle to pay international suppliers when hard-currency access tightens, a recurring issue in markets such as Nigeria. PAPSS addresses part of this challenge by enabling payments in local currencies and reducing dependence on foreign currencies such as the US dollar and the euro.

Regulatory Fragmentation

The third structural barrier is regulatory: 54 different regulatory environments mean 54 separate AML/KYC frameworks, 54 different cross-border payment approval processes, 54 different transaction limits, and 54 different reporting obligations, making cross-border expansion slow and expensive. A payment gateway that starts in Kenya often has to secure separate approvals, local banking relationships, and compliance coverage for each new market it enters, which makes regional scale feel more like a series of country launches than a single continental rollout.

No continental payments passport exists for Africa yet. Unlike the EU’s Payment Services Directive, which creates a single licensing framework across 27 countries allowing a licensed payment institution to operate continent-wide, African fintechs must license country by country.

The compliance and capital costs of multi-country licensing are significant barriers to the broad coverage needed to make intra-Africa payments genuinely seamless. This regulatory fragmentation is also a core reason the informal settlement layer (hawala networks, informal currency traders, and peer-to-peer mobile money workarounds) has been so persistent, despite the risks it poses to businesses that need audit trails, tax records, and trade-finance eligibility.

PAPSS: The Pan-African Payment and Settlement System

Of all the infrastructure being built to solve the intra-Africa trade payment problem, PAPSS is one of the most important and most frequently misunderstood. It’s important because it operates at the institutional layer, connecting central banks and commercial banks rather than serving businesses directly, and misunderstood because that institutional positioning means most businesses can’t access it directly, even though it’s the foundation that commercial gateways increasingly build on.

What PAPSS Is

The Pan-African Payment and Settlement System (PAPSS) is a Pan-African real-time gross settlement (RTGS) infrastructure for cross-border payments in distinct local currencies. It was publicly launched in January, 2022 by the African Union (AU) and the African Export-Import Bank (Afreximbank) to complement trading under the African Continental Free Trade Area (AfCFTA).

The ownership structure matters for understanding why PAPSS can do what it does. Afreximbank provides both liquidity support and a settlement backstop: if a member bank fails to settle its net position, Afreximbank covers the shortfall, giving member banks the confidence to participate without pre-existing bilateral correspondent relationships. The African Union provides the continental political mandate, and the AfCFTA secretariat has designated PAPSS as the official payment settlement mechanism for AfCFTA trade flows.

Four years after launch, coverage has continued to expand, with more countries, banks, and national switches coming online. That growth suggests PAPSS is moving from a policy concept toward real continental infrastructure, even though broad business-level access still depends on commercial gateways and participating banks.

How PAPSS Actually Works: The Technical Mechanism

Understanding the settlement mechanism explains both PAPSS’s strength and its current limitations.

The payment instruction is sent to PAPSS via the country’s central bank, which then routes it to the beneficiary’s bank account. PAPSS performs all validation checks on the payment instruction before forwarding it to the beneficiary’s central bank and eventually to the local bank account. PAPSS sends credit or debit settlement instructions to the Central Bank of the originator and the Central Bank of the beneficiary, with Central Banks settling the transaction in hard currency using Afreximbank as the settlement agent.

At the heart of PAPSS lies its multilateral net settlement framework, which reduces unnecessary currency exchanges. Instead of processing each transaction separately, it consolidates payments between countries and settles only the final balance.

For instance, if businesses in Country A export goods worth $10 million to Country B, while businesses in Country B export goods worth $8 million to Country A, PAPSS only settles the net balance of $2 million. This netting mechanism is what makes PAPSS cost-efficient at scale; the system dramatically reduces the total foreign currency required for settlement compared to the gross settlement of individual transactions.

On a daily basis, PAPSS settles the balances of all transactions among individual African currencies, netting them out before midnight. Central Banks then resolve the remaining difference, and the payments and settlement process starts again from net zero the next day.

The 2025-2026 Product Expansions: Three Major Launches

What changed significantly in 2025–2026 is PAPSS moving beyond the core payment rail into adjacent products:

PAPSSCARD

In 2025, Afreximbank, PAPSS and Mercury Payment Services launched PAPSSCARD, a continental card initiative aimed at reducing Africa’s reliance on foreign card networks. The goal is to keep more of the processing, fees, and data within Africa. This is significant: a Kenyan holding a PAPSSCARD can theoretically make purchases in Ghana or Rwanda without routing through Visa or Mastercard’s dollar-denominated processing infrastructure.

PAPSS African Currency Marketplace (PACM)

Launched in July 2025, PACM is a marketplace for the direct exchange of African currencies, designed to give businesses, banks, and institutions a more formal and transparent way to convert local revenues. It directly addresses the trapped-capital problem: airlines, multinationals, and other companies holding local currency in African markets can use a formal channel to exchange those balances instead of waiting for slow, expensive hard-currency conversions.

Nigeria-Ghana Wallet Corridor (February 2026)

In February 2026, Onafriq and PAPSS launched a bi-directional payment corridor between Nigeria and Ghana, described as Africa’s first wallet-based outbound payment pilot from Nigeria. It allows users to send money in naira and receive it in cedis, without using the dollar as an intermediary. This is architecturally significant: it connects mobile money wallets to the PAPSS rail for the first time, beginning to bridge the institutional bank-to-bank settlement system with the mobile money ecosystem that actually reaches most Africans.

PAPSS: The Honest Assessment

The future, experts say, lies in collaboration between regional systems and the continental PAPSS platform, which serves as a “network of networks” providing the final continental net settlement layer.

What PAPSS has genuinely achieved: as of 2025, PAPSS had expanded across four regions and connected roughly 18 to 19 countries, more than 150 commercial banks, and 14 payment switches. It has made meaningful progress toward reducing the need for intra-African bank-to-bank settlement to rely on external correspondent rails.

What PAPSS hasn’t yet achieved: despite the progress, everyday use still falls short of the promise. Some users continue to face delays, transaction limits, and low awareness. Those problems remain visible even in important corridors such as Nigeria and Ghana.

The gap between “PAPSS exists at the central bank level” and “an SME can easily pay a supplier in another African country through PAPSS” is still significant. Most businesses don’t access PAPSS directly; they transact through commercial banks, and many commercial banks haven’t yet fully implemented PAPSS at the customer-facing level.

The AI dimension is worth noting: PAPSS CEO Mike Ogbalu has said that modern payments are increasingly about data rather than physical cash, and that AI tools can help AML systems process large volumes of transaction data more effectively. If you use this in publication copy, it’s best to attribute the quote directly and keep the AI claim specific to the compliance functions the source actually mentions. The integration of AI into payment compliance infrastructure is directly relevant to the developments in the AI in Africa category that YourTechCompass tracks across the continent, and the regulatory dimensions of this AI deployment in financial services are covered in our AI policy in Africa guide.

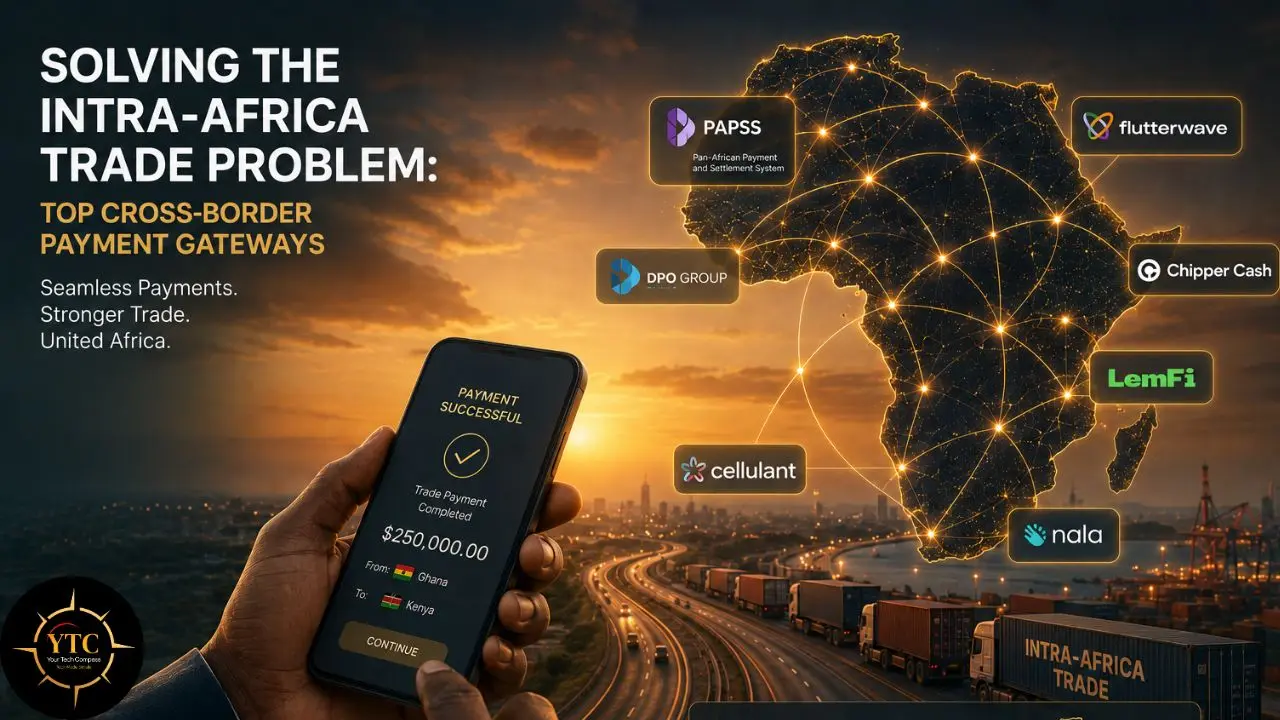

Top Cross-Border Payment Gateways for African B2B Trade

PAPSS is the institutional foundation, but most businesses need commercial gateway solutions they can integrate today, rather than waiting for banks to implement institutional infrastructure. Here are the top platforms operating across African B2B payment corridors.

1. Flutterwave: The Pan-African Gateway Leader

- Strongest Corridors: Nigeria-Kenya, Nigeria-Ghana, South Africa-East Africa, Nigeria-South Africa

- Typical Fees: Vary by country and payment method; published pricing shows local receiving fees that differ across markets.

- Best For: Businesses needing a single API for multi-market African payment collection and disbursement; e-commerce platforms; businesses with multi-country African footprints.

Flutterwave is one of the most geographically broad commercial payment platforms for African B2B trade, with coverage across many African countries and a single API for collections, transfers, and settlements.

For B2B specifically, Flutterwave handles invoice collection, multi-currency settlement, supplier disbursements, and payroll across most major African corridors via a single API integration. The January 2026 acquisition of Mono (Nigeria’s open banking data layer) deepens its B2B proposition by combining payment rails with financial data access, enabling credit scoring, account verification, and financial insights, all alongside payment processing, from a single platform.

Its recent stablecoin partnership with Polygon is strategically important for cross-border use because it introduces USDC and USDT settlement options on Polygon for corridors where local-currency transfer remains slow or expensive, especially in markets affected by FX restrictions. A business receiving payment in Nigeria may be able to use Flutterwave’s newer stablecoin rails for faster cross-border settlement in some cases, reducing reliance on legacy correspondent banking paths where supported.

2. Paystack: The Developer-First Gateway

- Strongest Corridors: Nigeria (primary), Ghana, South Africa, Kenya

- Typical Fees: 1.5% + local fee for domestic transactions; 3.9% for international card processing.

- Best For: Tech businesses, SaaS companies, and e-commerce operations primarily serving consumer markets in Nigeria and secondary West/East African markets; developers who want Stripe-quality API documentation and tooling.

Paystack was acquired by Stripe for approximately $200M in 2020 and has since expanded its African coverage while maintaining the developer experience quality that Stripe has standardized globally. Its January 2026 launch of Paystack Microfinance Bank adds licensed deposit-taking infrastructure to its payments stack, broadening its B2B proposition beyond checkout and payouts to a more complete financial services platform.

Paystack’s genuine strength is depth in specific markets rather than breadth across all of Africa: the Nigerian checkout experience is among the best available, with strong payment method coverage, high conversion rates, and mature fraud detection. Ghana is a key secondary market, while broader coverage across Africa remains more selective than that of a truly pan-African gateway.

3. Chipper Cash: The East-West Africa Bridge

- Strongest Corridors: Select East-West Africa corridors, including Kenya-Ghana, Nigeria-Uganda, Ghana-Tanzania, and Rwanda-Nigeria

- Best For: SMEs making regular, high-frequency cross-border payments between East and West African markets; businesses whose suppliers or customers span both the EAC and ECOWAS regions.

Chipper Cash holds a strategically distinctive position in the intra-Africa payment gateway market because it has meaningful coverage in both East Africa and West Africa, which is less common than it sounds. Many gateways are stronger in only one region, so bi-regional coverage makes Chipper Cash especially useful for businesses whose trade flows cross the traditional regional divide.

The business-facing tier operates on commercial pricing, distinct from the consumer-facing zero-fee model. The platform excels particularly for high-frequency SME payment flows (regular supplier payments, contractor disbursements, cross-border team payroll) where the combination of corridor depth and competitive pricing creates meaningful aggregate savings over time.

4. Nala: The FX Transparency Play

- Strongest Corridors: East Africa (Tanzania, Kenya, Uganda primary); UK/EU to East Africa

- Best For: East Africa-focused businesses; companies that prioritize FX cost transparency; procurement teams managing supplier relationships in Tanzania and Uganda specifically.

Nala built its reputation in diaspora remittances from UK and EU markets to Africa, particularly strong in the Tanzania, Kenya, and Uganda corridors, and has since developed a business-facing layer for cross-border B2B payments. Nala’s defining competitive positioning is FX rate transparency: mid-market exchange rates with explicit, published margins rather than opaque FX spreads embedded invisibly in the quoted rate.

For finance teams and CFOs at SMEs who need to accurately forecast cross-border payment costs rather than discover the true cost at settlement, this transparency is genuinely useful, not just a marketing claim. The ability to see the exact FX cost before initiating a payment changes working capital modeling and procurement decision-making in measurable ways.

5. LemFi: The Europe-Africa Bridge

- Strongest Corridors: UK/EU ↔ Nigeria, UK/EU ↔ Kenya, UK/EU ↔ Ghana

- Best For: African businesses with significant European revenue; firms managing multi-currency payroll for distributed teams across Europe and Africa.

LemFi holds a distinctive position in the Europe-Africa payments stack. In 2025, it received approval from the Central Bank of Ireland to acquire Bureau Buttercrane, inheriting a Payment Institution license that extends its regulatory reach across the EEA.

In April 2026, LemFi also announced a £100 million commitment to the UK and named London its global headquarters, reinforcing its Europe-facing operating base. That combination makes LemFi especially useful for African businesses that need to collect revenue in GBP or EUR and move funds into African markets without having to stitch together multiple providers.

For companies whose customers, investors, or partners are based in the UK or EU, including technology firms, professional services businesses, and exporters. LemFi can simplify cross-border collections and payouts by reducing the number of banking relationships involved. Its strength lies less in the depth of the broad African corridor and more in being a practical bridge between Europe and the African markets it already serves.

6. Cellulant (Tingg): The Mobile Money Aggregator

- Strongest Coverage: Kenya, Nigeria, Ghana, Tanzania, Uganda, Rwanda, Zambia, Zimbabwe, Ethiopia, Côte d’Ivoire, Senegal, Cameroon, and other African markets

- Best For: Agricultural businesses, FMCG companies, logistics firms, and multinationals with supply chains in mobile-money-heavy markets; businesses paying unbanked or underbanked individuals or SMEs across Africa.

Cellulant occupies a distinctive position in this comparison because it offers broad coverage of local payment methods, especially mobile money, across many African markets through a single API. Where some gateways are card-centric and add mobile money as a secondary option, Cellulant is better aligned with markets where mobile money is the primary payment rail and bank account penetration is lower.

For B2B businesses operating in Francophone West Africa, Central Africa, or East African markets, that matters a lot. Paying agricultural suppliers, artisans, distributors, or field workers often requires M-Pesa, Orange Money, EcoCash, or similar rails rather than card processing. In those contexts, Cellulant is often a practical choice because it reaches payment recipients through the methods they actually use.

7. DPO Group: The Enterprise Breadth Play

- Best For: Multinational enterprises, NGOs and development organizations operating across many African markets and established businesses prioritizing breadth of coverage and enterprise account management over individual gateway feature depth.

DPO Group, now operating under Network International following acquisition, positions itself as a broad African payment gateway with coverage across 54 African countries. For multinational enterprises, development organizations, and established businesses that genuinely need payment processing capabilities across the widest possible African footprint and prioritize enterprise-grade support and SLA commitments over gateway-specific features, DPO’s breadth of coverage is the deciding factor.

The trade-off is that the depth of coverage varies significantly across those 54 countries; availability in a country and the presence of deep, well-functioning local payment rails are different things. But for organizations whose primary requirement is “we need to operate formally everywhere in Africa,” DPO is the most comprehensive single-provider option available.

Gateway Comparison: Which Solution for Which B2B Use Case

Feature Comparison at a Glance

Provider | Coverage | B2B Invoice/Settlement | Local FX Settlement | Mobile Money | API Quality | Best Corridor Strength |

Flutterwave | Broad, pan-African coverage | ✅ Strong | ✅ Yes, plus stablecoin options emerging | ✅ Yes | ✅ Excellent | Nigeria ↔ Kenya, Nigeria ↔ Ghana |

Paystack | Select African markets, strongest in Nigeria | ⚠️ Stronger for merchant payments than cross-border invoicing | ⚠️ Limited | ✅ Yes in supported markets | ✅ Excellent | Nigeria-first |

Chipper Cash | Select East and West African markets | ✅ Business tier | ✅ Yes | ✅ Yes | ✅ Good | East Africa ↔ West Africa |

Nala | Core remittance corridors, especially UK/EU ↔ East Africa | ⚠️ Developing for business use | ✅ Transparent FX | ⚠️ Limited | ✅ Good | East Africa remittance flows |

LemFi | UK/EU ↔ Africa corridor strength | ✅ Yes | ✅ Yes | ⚠️ Not core | ✅ Good | UK/EU ↔ Africa |

Cellulant | Broad local-method coverage across many markets | ✅ Yes | ✅ Yes | ✅ Strongest | ⚠️ Moderate | Mobile-money-dominant markets |

DPO Group | Very broad formal African coverage | ✅ Enterprise | ✅ Yes | ✅ Yes | ⚠️ Enterprise-oriented | Broadest formal coverage |

PAPSS (via bank) | Institutional network across participating countries | ✅ Bank-level | ✅ Local currency settlement | ❌ Not a mobile-money gateway | N/A | AfCFTA institutional flows |

B2B Decision Matrix by Use Case

Business Scenario | Recommended Solution | Why |

Kenyan startup collecting from Nigerian clients | Flutterwave | Strong Pan-African collection/disbursement fit for Kenya-Nigeria cross-border use. |

West Africa e-commerce (card + mobile money) | Flutterwave + Cellulant | Flutterwave for broader card/cross-border coverage; Cellulant for deeper mobile-money rails. |

Francophone West Africa supplier payments | Cellulant / local mobile-money rails | Good fit where mobile money is more practical than cards or bank transfers. |

African tech business with EU/UK revenue | LemFi | Strong Europe-Africa bridge for GBP/EUR collections and African payouts. |

Multinational across 30+ African markets | DPO Group | Breadth of formal coverage and enterprise-style account management. |

Bank-to-bank settlement within PAPSS countries | PAPSS via member bank | Institutional local-currency settlement layer rather than a merchant gateway. |

East Africa SME supply chain payments | Chipper Cash | Good for recurring cross-border SME payments across East and West African corridors. |

High-frequency cross-border in EAC + ECOWAS | Chipper Cash | One of the better fits for businesses crossing the East/West regional divide. |

The Stablecoin and Blockchain Layer: The Emerging Settlement Rail

Stablecoins and blockchain-based settlement are not replacing traditional cross-border payment infrastructure in Africa, but they are filling specific gaps where traditional rails are genuinely too slow or too expensive. Understanding where this layer applies helps businesses route specific payment types appropriately.

The clearest use case is the naira corridor, where FX restrictions can create periods of hard-currency scarcity, delaying, making expensive, or temporarily blocking outbound payments from Nigeria through normal channels. In those moments, USDC settlement via blockchain rails can offer a faster and more transparent alternative outside the correspondent banking system, without the opacity and recourse gaps of informal channels.

Flutterwave’s stablecoin work with Polygon is one of the most important commercial signals in this area because it points to a model in which a business can initiate a payment via an API, settle part of the flow on-chain, and complete the local payout through a destination-side gateway. That does not remove all friction, but it can materially reduce settlement time in corridors where traditional channels are constrained. Grey Finance and similar platforms extend this model to accounts payable by helping African companies invoice in USD, collect via international transfer, and access funds through local payout channels.

The honest ceiling, however, is significant. Most African central banks have not formally approved stablecoins for regulated business payments, and regulatory, smart contract, custody, and counterparty compatibility risks all limit the layer’s applicability in formal business contexts.

For the large majority of African B2B trade, traditional gateway rails remain the operative infrastructure. The stablecoin layer is best understood as a corridor-specific alternative when conventional channels fail, not as a primary settlement rail for compliance-sensitive businesses.

Corridors: Where the Real Bottlenecks Are in 2026

Understanding which specific bilateral corridors are well-served versus underserved is more useful than headline country counts for business payment decisions.

Nigeria – Kenya: High Volume, Improving

This is one of the most important intra-African B2B corridors, driven by technology services, consulting, and trade flows between two of the continent’s most active business ecosystems. Historically, correspondent banking routes were expensive and slow, but commercial gateways have materially improved the experience in recent years.

The remaining bottleneck is naira convertibility during FX restriction periods. When it hits, even well-configured gateway routes experience delays or become temporarily unavailable through formal channels.

Nigeria – Ghana: Well-Served, Getting Better

Nigeria-Ghana is one of Africa’s most important bilateral trade corridors, especially for consumer goods and services. It is relatively well served by commercial gateways, and recent payment innovations are reducing reliance on dollar intermediation. The corridor is improving, but cost and reliability still depend heavily on FX conditions and the specific payment route used.

East African Community (Kenya-Tanzania-Uganda): Best Served in Africa

The East African Community is one of the most interoperable cross-border payment corridors on the continent. High mobile money penetration across Kenya, Tanzania, and Uganda, along with regional payment initiatives and mobile-money connectivity, has made this corridor more practical than many others for everyday cross-border transfers.

In some cases, mobile money transfers can be materially cheaper than legacy correspondent banking routes, especially for smaller payments. Nala and Chipper Cash add more options for users seeking competitive cross-border transfer routes, though the best route still depends on the payment method, amount, and corridor conditions. This corridor is a useful reference point for what better regional payment interoperability in Africa can look like.

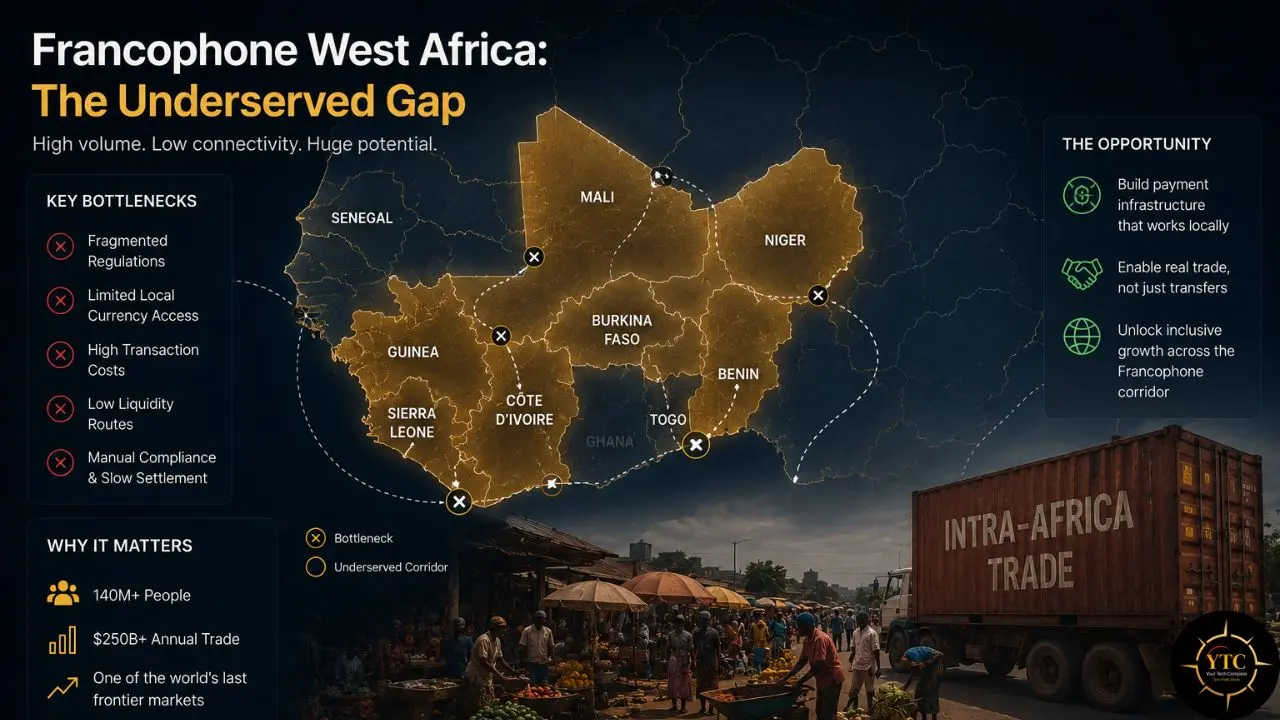

Francophone West Africa: The Underserved Gap

The CFA franc zone is relatively low-friction internally because WAEMU and CEMAC member countries share currencies pegged to the euro, which reduces intra-zone FX complexity. The bottleneck appears at the border between Francophone and Anglophone Africa: paying a Nigerian supplier in Côte d’Ivoire or a Kenyan partner in Senegal still often involves the full cost and complexity of cross-border settlement.

Mobile money, including Orange Money, MTN MoMo, and Wave, plays a much larger role than cards or bank accounts in many of these markets, which is why mobile-money aggregation models are often more practical than card-centric gateways. Cellulant’s coverage of local payment methods makes it one of the more useful options in this region, especially for businesses that need to pay suppliers, agents, or field workers via mobile money rather than card infrastructure.

South Africa to Sub-Saharan Africa: One-Way Friction

South Africa’s rand is more freely convertible than most African currencies, making inbound payments to South Africa from most African countries relatively straightforward. The friction is outbound: paying from South Africa into restricted-currency markets (naira-denominated payments in Nigeria, Ethiopian birr-denominated payments) entails the same correspondent banking complexity and FX-restriction exposure as any other corridor involving those markets. Stitch’s open banking infrastructure handles the South African side well; the destination-side complexity is the unresolved variable.

What B2B Businesses Should Evaluate Before Choosing a Gateway

Seven practical factors that determine whether a gateway will actually work for your specific business, rather than for the general market it claims to serve:

1. Corridor-Specific Coverage, Not Headline Country Counts

A gateway claiming “34 countries” is only as useful as its depth in the corridors your business actually uses. Verify the available payment methods in each destination and determine whether the coverage is primary or thin. Flutterwave’s 34 countries include markets where coverage is deep and markets where it’s thin; know which category yours falls into.

2. Local Payment Method Acceptance At Destination

For many African markets, “accepting payments” means accepting mobile money. Confirm the gateway supports M-Pesa, MTN MoMo, Orange Money, or whichever platform your specific counterparty uses, not just bank transfer and card acceptance, which may be inaccessible to your actual partners.

3. All-In Cost, Not Just Quoted Fee

Some gateways quote zero transfer fees but embed margin in the FX rate, which is often more expensive than an explicit fee at the mid-market rate. Compare the total all-in cost (fee + FX spread) at your specific transaction volume. Request quotes with explicit exchange rates rather than accepting “competitive rates” as an answer.

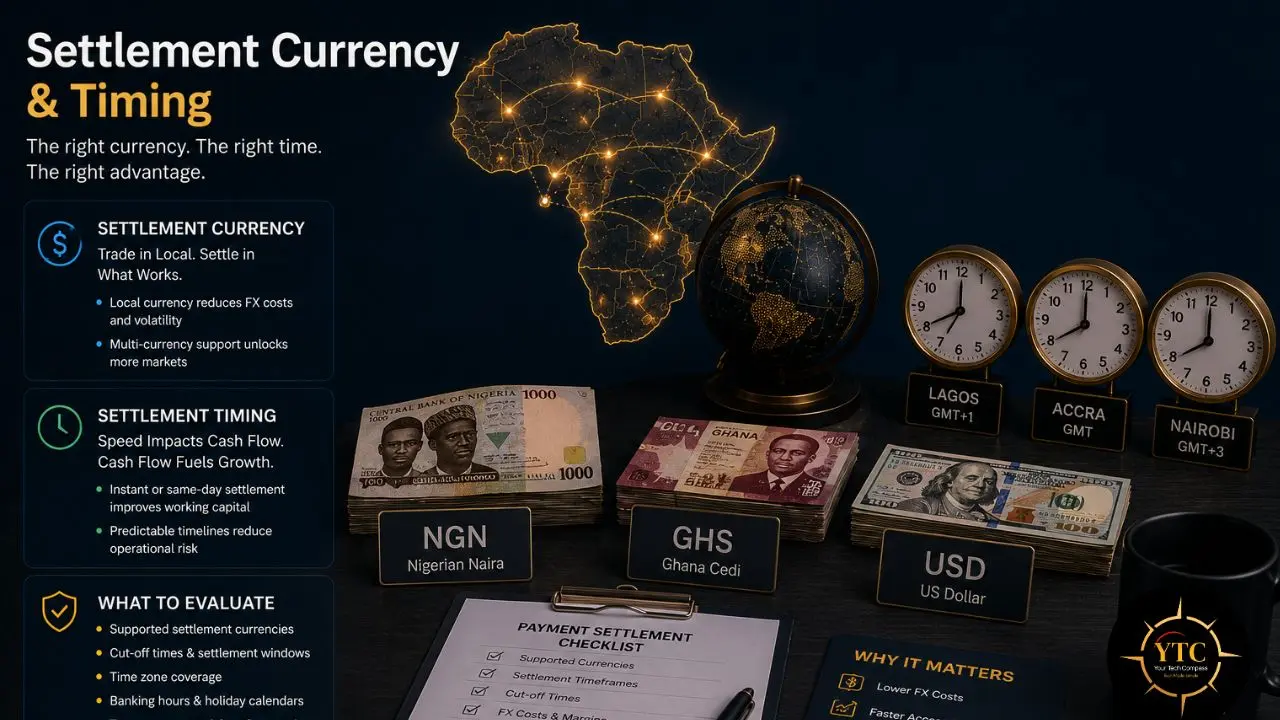

4. Settlement Currency and Timing

Can you settle in local destination currency, USD, or your home currency? How long does settlement take in each specific corridor? For working capital management, settlement timing matters as much as cost; a 3-day delay in supplier payment settlements can create procurement bottlenecks regardless of the fee structure.

5. Regulatory Compliance Infrastructure

Confirm that the gateway has regulatory approval in every country where you need to operate, and determine whether specific corridors impose transaction limits or additional compliance requirements that could constrain your payment volumes as you scale. This is particularly important for corridors involving Nigeria and Ethiopia, where regulatory complexity is highest.

6. Transaction Volume Tiers

Most gateways offer better pricing at higher transaction volumes, and enterprise pricing negotiation is often available above certain thresholds. Understand the volume tiers and where your current and projected transaction volumes sit, then negotiate.

7. Failed Transaction Resolution

This is the most important factor and the least covered in marketing materials. What happens when a payment gets stuck, which happens more often in African corridors than in developed-market rails? What is the documented resolution time and SLA for failed transactions in each specific corridor? Ask for this before signing, not after experiencing your first stuck payment.

The broader fintech infrastructure context for these gateway decisions (funding landscapes, hub dynamics, infrastructure layers) is covered in our African Fintech Ecosystem Guide. Profiles of the most consequential fintech startups building cross-border payment solutions are included in our African Fintech Startups to Watch 2026 guide.

The full historical context of mobile money that underpins current cross-border infrastructure is covered in our mobile money evolution in Africa guide, and our mobile money Africa guide covers current use cases. For Nigeria-specific digital lending in the context of cross-border trade finance, our digital lending Nigeria guide is directly relevant.

Furthermore, our DTB Wearables Kenya review covers an example of the contactless payment infrastructure extending the payment rail into everyday consumer touchpoints, the consumer-layer complement to the B2B infrastructure covered here. The full African Fintech category on YourTechCompass tracks all developments in this space.

The AfCFTA Opportunity: What Better Payments Would Actually Unlock

The World Bank projects that full AfCFTA implementation could increase African GDP by $450 billion by 2035, but that projection is explicitly conditional on trade barriers being genuinely reduced, and payment friction is one of the most significant remaining trade barriers. The policy intent (AfCFTA) and the payment infrastructure (PAPSS + commercial gateways) are two legs of the same table. Without functional payment infrastructure, trade liberalization remains aspirational.

What genuine AfCFTA-enabled payment infrastructure would specifically unlock for African businesses: the ability to issue invoices and receive payment in African local currencies rather than requiring USD as an intermediary, removing the FX risk that currently sits with both parties in most intra-African B2B transactions. The ability to access trade finance secured by African payment rails rather than requiring US or European bank guarantees, currently a significant constraint on SME growth that depends on cross-border trade.

Reduced working capital locked in FX conversion timing and correspondent banking settlement delays. And fundamentally, more trade that currently simply doesn’t happen because the payment friction makes the economics unviable.

The reality of the timeline is important to hold alongside the optimism: the infrastructure being built now; PAPSS’s 19-country coverage; Flutterwave’s banking licenses; Paystack’s MFB; the February 2026 Nigeria-Ghana wallet corridor; and stablecoin rails filling corridor-specific gaps represent the first generation of genuinely Pan-African payment infrastructure. PAPSS is not just connecting banks; it is creating a framework to link different regions, national switches, and the next generation of financial services, including mobile money operators and wallets.

Full AfCFTA payment integration will likely take years, not months. But the foundation is being laid with meaningful institutional commitment and commercial investment, which is a materially different situation from five years ago.

FAQs

It depends heavily on the corridor. In the East African Community, mobile money-based services such as M-Pesa and some wallet aggregators can be among the lowest-cost options for certain transfers. In PAPSS-enabled corridors, local-currency settlement can reduce correspondent-banking friction and may be cost-efficient for formal bank-to-bank payments. For Nigeria-facing corridors, some commercial gateways and wallet rails can be competitive, while in Francophone West Africa, mobile-money aggregation is often more practical than bank-led transfer routes where mobile money dominates. The best practice is to compare the all-in cost (fees plus FX spread) from at least two providers for your exact corridor and payment size.

PAPSS is a centralized Financial Market Infrastructure that enables the efficient, secure flow of money across African borders, minimizing risk and contributing to financial integration across regions. Your business doesn’t access PAPSS directly; you access it through member commercial banks that have connected to the PAPSS system. Ask your business bank whether they are a PAPSS member (particularly if you’re in Nigeria, Ghana, Kenya, Rwanda, or South Africa, where member bank coverage is strongest). If they are, PAPSS-routed cross-border transfers to other member country accounts may be cheaper and faster than traditional correspondent banking alternatives.

There is no single best gateway for all African cross-border payments. The right choice depends on your corridors, payment methods, settlement needs, and whether your flows are card-based, bank-based, or mobile-money-based. Flutterwave is often a strong fit for businesses that need a single API across multiple African markets. Cellulant is especially useful for supply chains and payouts in mobile-money-dominant markets. LemFi is a strong option for Europe-to-Africa payment flows and disbursements. Paystack is best suited to Nigeria-focused, consumer-facing businesses. Therefore, use a corridor-by-corridor decision matrix, not brand reputation alone, to identify the best platform for your specific payment flows.

Increasingly, yes, but only in certain corridors and through participating institutions. PAPSS and related regional payment rails have made local-currency cross-border settlement technically possible in more African markets, reducing the need to route every payment through USD or other hard currencies. For businesses trading in PAPSS-enabled corridors, local-currency invoicing and settlement can reduce FX exposure, reduce dependence on correspondent banking, and simplify cross-border trade operations. But for restricted currencies and markets outside the supported network, USD invoicing and destination-side conversion still remain the most practical setup for many companies.

Francophone West Africa has a distinctive payments landscape. Inside the WAEMU zone, businesses share the West African CFA franc, which keeps many intra-zone payments relatively low-friction compared with cross-currency corridors. The main complexity starts when businesses need to pay outside the zone, for example into Nigeria, Ghana, East Africa, or global supplier networks, where FX conversion, bank routing, and compliance requirements reappear. Mobile money is often one of the most practical rails in these markets, so gateways with strong mobile money aggregation capabilities can be more useful than card-centric providers for supplier payouts, agent payments, and smaller B2B transfers. In practice, businesses should confirm support for the local platform their counterparty actually uses, especially Wave, Orange Money, or MTN MoMo depending on the market.

Four specific risks deserve attention. First, FX restriction risk, particularly for the Nigerian naira corridor, where central bank policy changes can temporarily block outbound payments through formal channels. Second, settlement delay risk: even well-rated gateways experience corridor-specific delays during high-volume periods or due to regulatory compliance holds; build settlement timing buffers into supplier payment terms. Third, compliance and documentation risk: cross-border payments above certain thresholds require supporting documentation in most African markets; missing this documentation can cause payment holds that are expensive to resolve. Fourth, gateway concentration risk: businesses routing all cross-border payments through a single gateway have no alternative when that gateway experiences downtime or corridor-specific issues; maintaining relationships with two gateway providers for key corridors provides operational resilience.

Conclusion

The intra-Africa trade payment problem is measurable and consequential: Sub-Saharan Africa remains among the world’s most expensive regions for cross-border transfers, and that cost burden reduces working capital, delays settlement, and makes some trades uneconomic. PAPSS is forecast to save the continent more than $5 billion annually once fully operational. Those are not abstract numbers; they represent capital that could otherwise support trade, investment, and hiring if moving money across African borders were less expensive and less fragmented. The infrastructure being built to close that gap is further along than most international business coverage acknowledges. PAPSS has moved from concept to an expanding institutional settlement network, while commercial gateways such as Flutterwave, Paystack, Cellulant, and Chipper Cash have built a practical layer for corridors that PAPSS does not yet fully reach. Together, they have made cross-border payments in Africa more workable than they were five years ago, even if the system is still uneven.

That progress has not eliminated the problem; it has begun to solve it, corridor by corridor, institution by institution. The businesses that navigate this landscape best are not waiting for perfect infrastructure. They are mapping payment flows to actual corridor coverage, comparing all-in costs rather than quoted fees, using multiple providers where needed, and building payment resilience into their operating model instead of discovering corridor-specific gaps during a live transaction. The AfCFTA’s GDP opportunity will be easier to capture if businesses learn to move money across African borders efficiently now, not after the infrastructure is perfect. The tools exist. The infrastructure is maturing. The question is whether your business is using what is already available.

African fintech is one of the fastest-moving spaces in global technology and commerce. Visit YourTechCompass.com for ongoing coverage of payment infrastructure, fintech startups, and the tools shaping how money moves across Africa.